Visa: Two Years Later – A Retrospective and a Look Ahead

Turning Projections into Profits: How Visa Delivered Big Over Two Years

Just over two years ago, I wrote my very first rundown of a company and the investment options I was considering. I chose Visa because it’s a great company with a strong track record. It also has a consistent valuation, a solid growth model, and trades at a high earnings multiple—all good qualities. It’s an excellent company to own as underlying stock and seemed to have potential for long calls as well. When I looked into it, Visa did indeed offer LEAPS, and they were trading at low implied volatility (cheap). Putting it all together, I made my first post.

It was a simpler time back then. I had no fun photos, my charts were uglier, and I didn’t have a way to proofread anything. The numbers and projections, however, were solid. Now, as an AI junkie who makes photos and lets the future rulers of the world clean up my typos, my method for doing the cold, hard math remains the same. It worked then, and it will work now.

This is my first time coming to the end of the road with a stock, and in some ways, this post is very similar to my recent "The End Nears" piece. That one focused more on tax strategy and next steps, while this will be a reflection on my original projections and another look ahead.

A year in, I posted an update where we liked what we saw. In that update, I added two more options to our scoreboard. Both have performed quite well, and I think I’ll be adding January 2027 calls to the board as well. Before we dive into that, let’s step back to Thanksgiving 2024. We’ll review what I predicted, how it played out, and then take another look forward to see what the future may hold.

Turning back to November 2022

Two years ago, Visa’s stock was trading at around $211 per share. It had been doing what it always does—growing at a decent clip, from $37 to $211 over 10 years. However, it had stalled out during the post-pandemic inflation and recession concerns of 2022. At the time, I wrote:

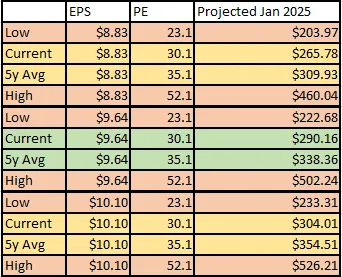

“Visa currently trades at a trailing 12-month (TTM) PE of 30.1 with TTM earnings of $7.00 per share. Over the past five years, it has averaged a PE of 35.1. In the past eight years, the highest PE it has ever reached is 52.1, and the lowest is 23.1. In recent history, anywhere from 28–35 for a PE is standard. Due to inflation concerns, things stand at the low end of that ratio even as earnings continue to rise in recent quarters.”

I used analysts' estimates for earnings for the fiscal year ending September 30, 2024, to model some likely outcomes for the stock’s performance. I also noted the advantage of having a few months beyond that date for the option expiration. Based on those numbers, I built the table below:

There were a wide range of potential outcomes, but I focused on the green numbers in the middle of my projections. As we approached the option’s expiration date, I expected Visa to trade in the range of $290.16–$338.36. Back then, I was more optimistic than most about inflation and felt confident in a company like Visa, which has historically performed well through various economic cycles.

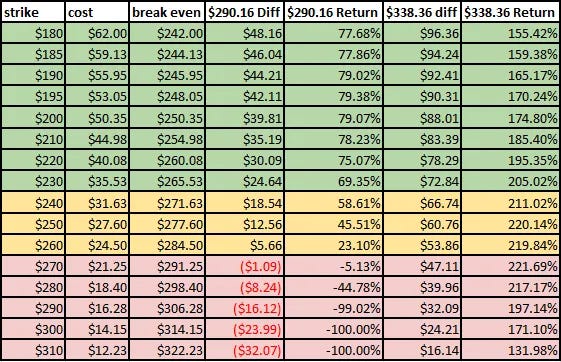

With those numbers in hand, I turned to the options available at the time. I applied the most likely range I modeled to the LEAPs expiring in January 2025 and created the following table:

This table highlighted the strikes available near the then-current price of $211, their cost, the breakeven price by January 2025, and the potential returns at $290 and $338. In a scenario where Visa traded at $290, many strikes offered around a 78% return, while the more expensive strikes provided even better returns the further out of the money they were.

I identified the sweet spot at $210 strikes, priced at $44.98. This offered nearly 80% returns on the lower end of my likely range and up to almost 200% on the higher end. This position became the first for Rolling Thunder.

The Present

Today, Visa is performing quite well. Since my post on November 20, 2022, the underlying stock has climbed from $211 to $315. Compared to my modeled range of $290–$338, that’s pretty impressive. The midpoint of my range was $314, and with less than 48 days to go, we’re just $1 off that target. Solid.

The chart below illustrates Visa’s journey since opening this position.

This means our $210 strike options, purchased for $45, are now worth approximately $106.70—a total return of 137%, or 53% annualized. Visa ended up earning $9.92 per share for the year ending September 30, 2024, which falls within the modeled range of $8.83–$10.10 but slightly above the predicted $9.64.

We modeled PE ranges of 30.1 to 35 for our price range, and Visa currently trades at a PE of 32.3. All this is to say, based on what we predicted, we did quite well. Our returns land right in the sweet spot of our projection range: between 80–180% over two years.

The first Rolling Thunder position was a slam dunk. The range we modeled for the stock was accurate for all the right reasons, and as a result, our option has appreciated handsomely.

The Revisited Options

A year in, I outlined additional options that seemed like winning plays—one being another strike for January 2025 and another for January 2026. So, how do those look now?

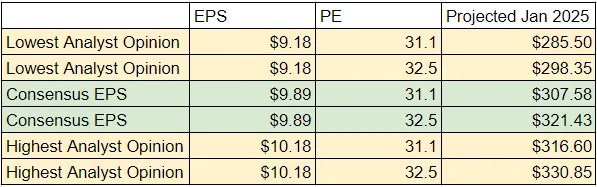

So far, so good for those positions. In the "One Year In" post, I tightened the window of expectations to:

I wrote then:

“Anticipating a potential Fed interest rate cut next year, there's a chance the PE could expand in response. However, it seems unlikely to reach a 35 PE for Visa, especially considering the 5-year average PE dropped to 34.3 in the past year. Given Visa's widespread coverage and consistent track record, earnings are expected to align closely with the consensus. It's worth noting that despite analysts' average price target of $284 a year from now, recent Fed activity hasn't been factored into those estimates.”

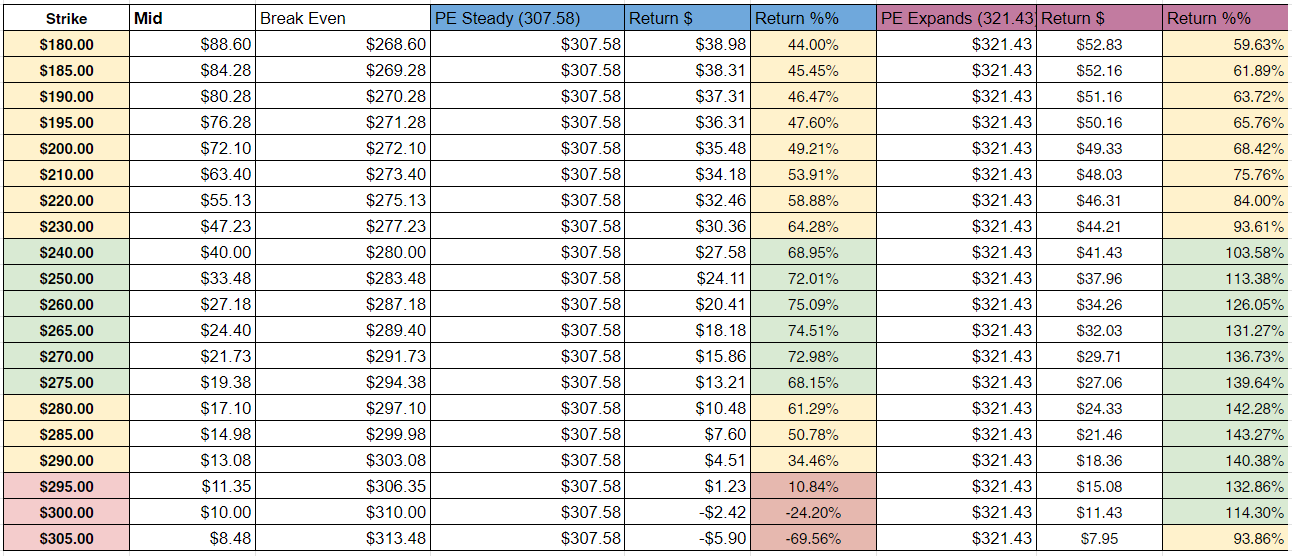

As the year comes to a close, the $307–$321 expectation also appears to be spot on, making the options prices at the time—and my modeled returns—seem rather prophetic.

What looked like it would be a free double did, in fact, turn out to be one! It's a testament to the importance of following where the numbers lead. That’s a key lesson from evaluating January 2025 in December 2023. I projected $20–$40 growth based on earnings expectations, which made sense—and turned out to be correct. That expectation translated into a free double.

With interest rate changes uncertain and the upcoming election adding to the murkiness, I projected a much wider range for my 2026 expectations and the option I added for that year. I did my best to model the possibilities and arrived at:

My thinking at the time was that $347–$379 seemed like the more likely outcomes. This made it an easy decision to add a 2026 option to the board, which, as we saw above, is performing exceptionally well so far!

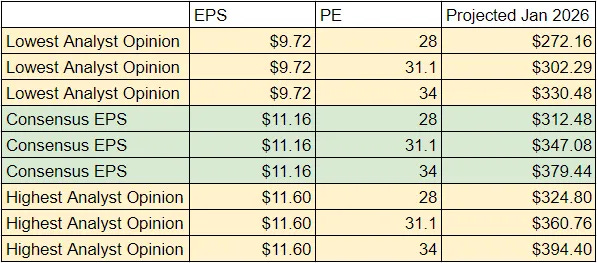

What would I expect for 2026 today? I can update my previous table with more current numbers. I still like a 31 PE for my lower band, but as Visa's five-year average PE continues to decline, I’d likely adjust the upper band to 33.5. The current TTM PE of 32.3 sits comfortably in the middle of this range.

These are my updated Visa stock projections for January 2026. Would it make sense to buy more options for next year, based on these numbers and the current option prices?

At the lower end of that band, you would just break even, while the upper end offers a 70% return. That’s not something I would be interested in. Since call options can expire completely worthless, I avoid scenarios where the lower end of my likely return band is near 0%. At that point, I’d rather buy the underlying stock if I believe in it or look for better opportunities elsewhere.

For now, I’d hold onto the 2026 option I added to the board last year if I were to own it. It’s so far in the money that it’s like playing with house money, and it could still have some room to grow. More importantly, it’s just a few weeks shy of reaching long-term capital gains territory. Once it crosses that threshold, I’ll reassess and update you.

The Distant Future!

Lastly, we need to look ahead to January 2027. What do we think Visa will trade at by then? Will any current options make sense as new holdings for the scoreboard? Let’s take a look.

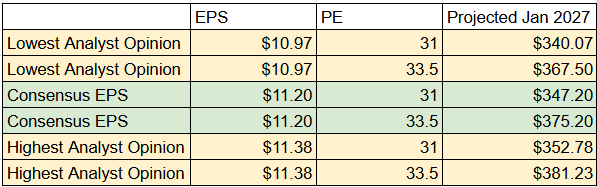

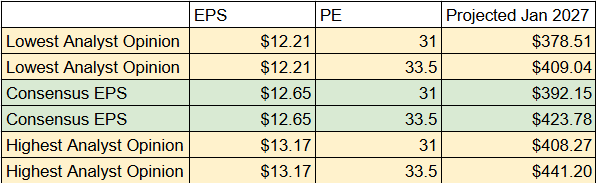

For the year ending September 30, 2026, Visa’s earnings expectations range from $12.21 to $13.17, with a consensus of $12.65. It remains highly covered, with 34 analysts contributing to that range, which passes the sniff test for me. Over the past five years, Visa’s EPS growth rate has been just under 13%, and it’s expected to remain at about 13% for the next five years. As they say, that maths.

Taking this year’s $9.92 EPS and applying two years of 12.9% growth gives us $12.64—right in line with consensus estimates. Using that EPS and the same PE range as above (31–33.5), we can project forward and expect:

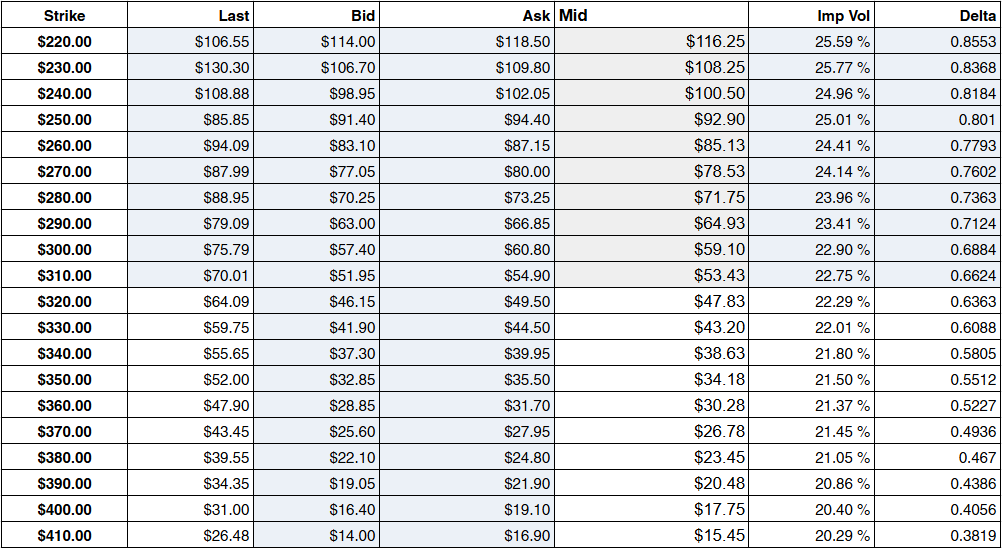

For two years out, that’s a relatively narrow band, but I don’t see any reason not to start there. I’m going to post a picture of the current call option prices for January 2027, followed by a table outlining potential returns if either of the green-highlighted stock prices above comes true.

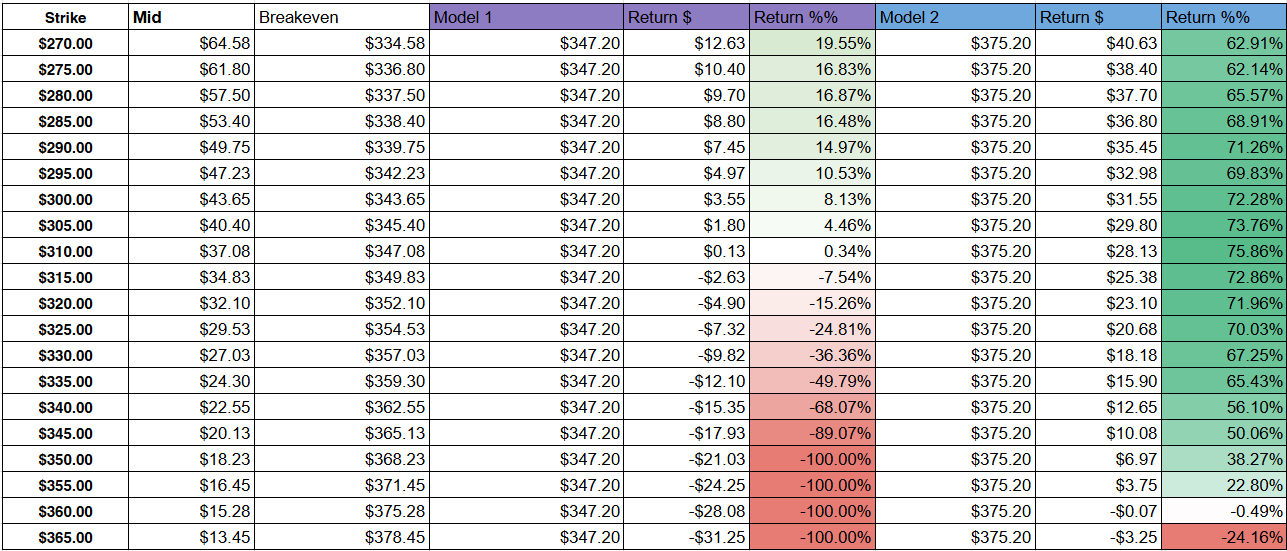

Option Prices

Modeled Outcomes

Looking at our modeled outcomes, things look much better than the updated 2026 options. We’re aiming to turn fairly standard Visa performance into a 50–110% return. The sweet spot for the lower end of the expected outcome appears to be in the $240–$320 strike range, all of which would yield around 50% returns.

On the higher side of expectations, there are numerous strikes that could return north of 110%. While I find this investable, it’s near the lowest end of what I consider acceptable. With the wipeout risk of options, I aim for solid chances of doubling returns. The sweet spot here seems to be the $300–$360 strikes. Among these, the $300 strike offers better returns if outcomes trend toward the lower end of expectations, while the $320 strikes provide greater upside if things outperform.

In this case, I’ll take the Goldilocks approach and put the $310 strike options for Visa January 2027 on the scoreboard! This will be our 21st position.

Summary

Visa has been good to us, and as long as it remains the predictable, profitable payment giant it is, I’ll continue to explore LEAPS opportunities with it. As things stand today, the potential returns are lower than they were two years ago but still attractive enough to consider.

Additionally, I’ll use this post as the closing point for the Visa options expiring in January 2025. For me, this feels like a good time to exit. With just seven weeks left, I’m satisfied with the return. Realistically, there’s not much more meat left on these bones, but there’s always the risk of the underlying stock declining.

Depending on your situation, your choices may vary. You can refer to the strategies discussed in The End Is Near post: sell in 2024, sell in 2025, exercise now and sell in 2025 to lock in today’s price, or exercise and hold the underlying stock. The best path forward is the one that aligns with your individual needs.

I hope this has been both helpful and informative.

Happy Investing,

S. Andrew

*Nothing sent out is meant to be financial advice, invest at your own risk.*

Disclaimer:

The information provided in this newsletter is for educational and informational purposes only and does not constitute financial or investment advice. Options trading involves significant risk and is not suitable for all investors. It is possible to lose all or more than your initial investment. Please consult with a licensed financial advisor or other qualified professionals before making any investment decisions.

Assume the author currently holds options positions in all the securities discussed in posts or listed on the scoreboard. These holdings may influence the opinions and analysis presented in this newsletter. This disclosure is provided to maintain transparency and should not be considered a recommendation to buy or sell any securities.

Any projections, forecasts, or examples provided are hypothetical and for illustrative purposes only. Past performance is not indicative of future results. While every effort is made to ensure the accuracy of the information, it is not guaranteed to be complete, accurate, or up-to-date.

Links to third-party websites are provided for convenience only. The author does not endorse or take responsibility for the accuracy of third-party content. All models, tools, and content provided are for personal use only and may not be reproduced, distributed, or used for commercial purposes without permission.

The author assumes no responsibility for any losses incurred as a result of using the information provided in this newsletter. By reading this newsletter, you agree to these terms.