The End Nears…

Our Initial Options Expire in 3 Months

It's been nearly two years since this Substack began. In that time, I've written about over 20 options plays and a sector-targeted bank trade. While most of the positions I’ve covered have over a year left, my initial three LEAPs—American Express, Visa, and Mastercard—expire in January. This brings us into a topic I haven't covered much yet: how and when do we exit? As with many aspects of investing, there isn't a single "right" answer that applies to everyone. However, there are a few key factors that everyone should consider when making their decision.

The Options for our Options:

The first thing to review is our options—pun intended. All three of these plays have performed quite well: we’re up 57% on Visa, have doubled with a 108% gain on Mastercard, and tripled with a 252% gain on American Express. This means it’s highly likely these options will expire in the money by January. So, what happens when an option expires in the money? It gets exercised.

For all three of these calls, the holding period qualifies them for long-term capital gains treatment, assuming they were purchased and held in a taxable account. If bought within a tax-sheltered account, of course, you won’t owe taxes on the gains. This brings up other considerations: when do you want to log your gains, and do you have enough capital to exercise the options—or do you even want to?

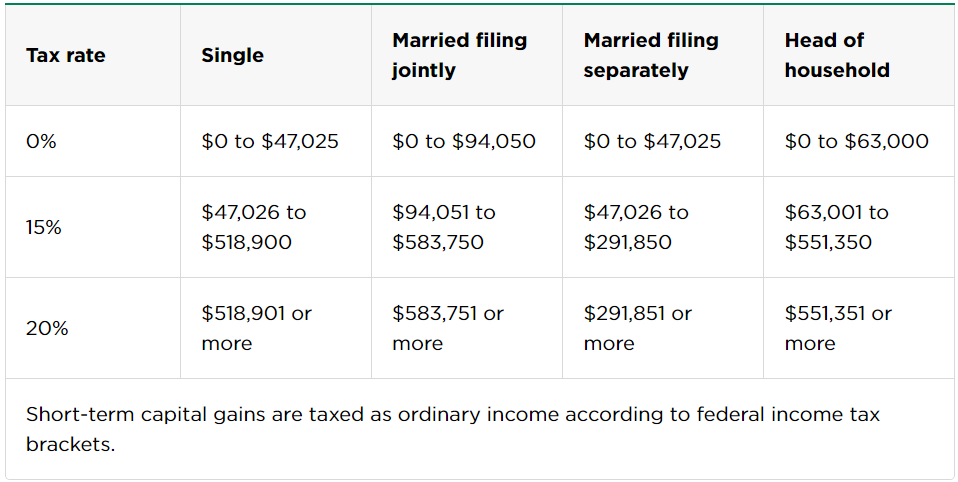

For anyone unfamiliar with the details, here’s a handy chart from NerdWallet on long-term capital gains.

Exercise:

The case for exercising is pretty straightforward. If you exercise the option, you’ll need to come up with the funds to purchase 100 shares at the strike price, but exercising itself doesn’t trigger any taxation. For example, if I have the AXP call in a taxable account and decide to sell it, I would trigger over $6,500 in taxable gains, losing 15% of that to Uncle Sam—around $1,000. That’s money I’d obviously prefer to keep for myself.

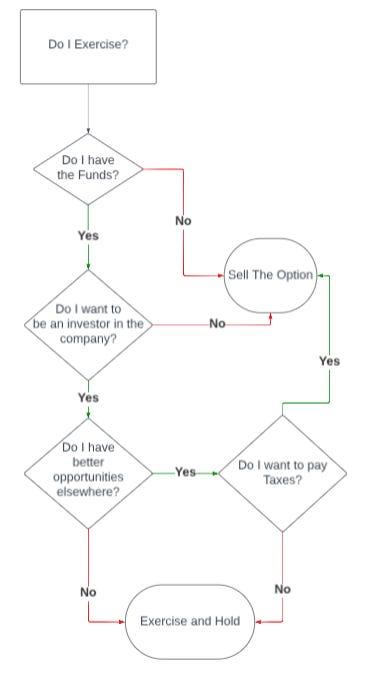

If I like American Express as a company and believe it will continue to grow at a solid pace, I’d consider holding the underlying shares and avoiding the immediate tax hit. However, I’d need to come up with $18,500 to exercise the option. Additionally, I’d need to think about whether I could deploy that capital in better investments elsewhere. Here’s a simplified way I approach this decision, charted below:

The most important question to ask is: Do I have better opportunities elsewhere? This question will guide whether you want to pay taxes or keep the underlying stock. It’s a decision I hope to answer for both myself and for you this fall. In September, the January 2027 options were released, and fall is the time of year when I reassess my portfolio and plan out which options I want to pursue. Through my posts, I hope you'll be able to answer that question for yourself before you need to make a decision.

Sell in 2024

Another option is selling in 2024. In this case, you would trigger capital gains for 2024, which will show up when you file your taxes next year. Each of the credit card companies will report one more quarter of earnings before year-end, and since they are all in the same sector, they’ll likely face similar positives and negatives. Generally, I prefer to hold longer, as another quarter of growth will likely benefit the stock prices. If you’re happy with the returns so far, you might want to lock them in now just to be safe. Otherwise, waiting until November or December to close things out could make sense.

Using American Express as an example again, the $185 strikes are currently trading at a mid-price of $94. That combined with the underlying stock price of $276.16 gives you a total of $279, with about a $3 difference as time value for the remaining 90 days. The question to ask here is: Do I think the stock will grow more than 1% over the next 90 days? If yes, holding longer makes sense. But if you expect the stock to stay flat, or you’re ready to call it a day, exiting sooner may be the better choice.

As with exercising, ask yourself a few key questions: Do I expect stock growth? Do I want to deal with earnings volatility? Am I satisfied with my current return? Do I have other losses to offset my gains? These questions will help you decide when, in the next three months, you should sell.

Sell in 2025

If you’ve already made some extra money this year, had a windfall, or just don’t want to increase your 2024 tax bill, holding these options until January might be your best move. By doing so, you’ll defer paying taxes on the gains until you file for 2025 taxes in 2026. In effect, you’ll have what amounts to an interest-free loan from the government for a year, which you can use however you like—whether it’s reinvesting, saving, or even withdrawing it just to look at! Any money not owed in taxes is truly yours to do with as you please.

Once you decide on this path, there’s very little to worry about. There are roughly two weeks in January before these options expire, and during that time, the option price plus the strike price will closely approach the stock's daily trading price. At that point, I typically find a convenient day after the New Year to close out the positions I don’t plan to exercise, without stressing too much over the timing of the exact day.

Summary

Now is the time to start thinking about what you want to do with any of these options you’ve bought into. I’ll be doing the same. There are only three choices, but each one has its merits depending on your situation. As fall progresses, I’ll be sharing my new ideas and writing a close-out piece for these positions. For now, my plan is to hold through earnings and reassess from there. Another factor to consider is the likelihood of a rate cut this fall, maybe even more than one. That would boost the stock prices of all the credit card companies. It’s another reason to play wait and see before making a decision later this year.

Happy investing,

S.