Starbucks (SBUX)

We've got a hot one here! And I'm not just talking about the drinks. Starbucks, the iconic coffee chain, is looking ripe, and I'm here to break down why!

Background

One of America’s largest chains, Starbucks, is nearly ubiquitous across the country. Known for its higher-end coffee and fast food service, it's like a McDonald's that makes you feel fancy. Despite reporting record earnings in late November, the stock is currently near its one-year low point, down over 10% from the previous year. This is peculiar considering the expected 17% growth in earnings in the coming years. So, let’s grab a coffee, sit back, and delve deeper.

Performance

Over the past 5 years, Starbucks has experienced a substantial growth of approximately 40%. However, the last 3 years have shown a relatively stable performance for the company. Despite this, there is an ongoing expansion, with plans to add 17,000 stores worldwide by 2030, coupled with a consistent rise in same-store sales. In the final quarter of 2023 alone, same-store sales witnessed an impressive 8% increase. Despite these positive indicators, there appears to be a disconnect with the stock price. Some third-party reports suggest a potential slowdown in sales for the upcoming holiday season, but this may be perceived as an overreaction.

Expectations

Building on the topics above, let's delve into the expectations. The company is expanding by adding stores, increasing earnings, and initiating share buybacks. In the fall of 2021, it authorized a $20 billion program for dividends and buybacks. With the current stock price valuing the company at $105 billion, assuming 2/3 of the authorized amount has been used, approximately 7% of the company’s total value is projected to be distributed to shareholders this year – 2.5% as dividends and 4.5% as buybacks.

Over the next 3-5 years, earnings are anticipated to grow at a robust 17%. The fiscal year for Starbucks concludes in September 2024. Analysts, numbering 33, expect earnings to increase from 2023’s $3.54 to $4.13, marking a 16.7% rise. Projections for the year ending 9/30/2025 indicate earnings of $4.82 (another 16.7% increase). Given the company's historical performance, strategies for new stores, same-store sales growth, and share buybacks, achieving these targets seems plausible. Surpassing expectations wouldn't be surprising.

Company management has provided guidance of 15-20% earnings growth, driven by 5-7% comparable sales growth and 10-12% revenue growth. Additionally, their consistent local success is a testament to their operational strength.

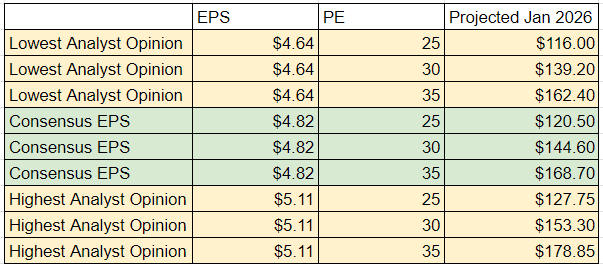

Now, considering the earnings numbers above, what would the stock be worth in 2 years? The critical factor is the Price-to-Earnings (PE) ratio. Starbucks has historically traded between 25-35 (excluding Covid), but given recent market trends, a PE range of 25-30 seems more realistic. Assuming a smooth execution of plans, a PE around 30 seems probable as the company's growth rebounds. Plotting these earnings and PE ratios on a chart, we can explore potential stock values.

That is a significant spread! One thing is for certain – with the anticipated growth in earnings, all price-to-earnings ratios (PEs) seem favorable from a base gain perspective, including the lowest EPS with the lowest PE. Let's take a look at the options for January 2026 and examine the potential returns for the green center of EPS across various PEs.

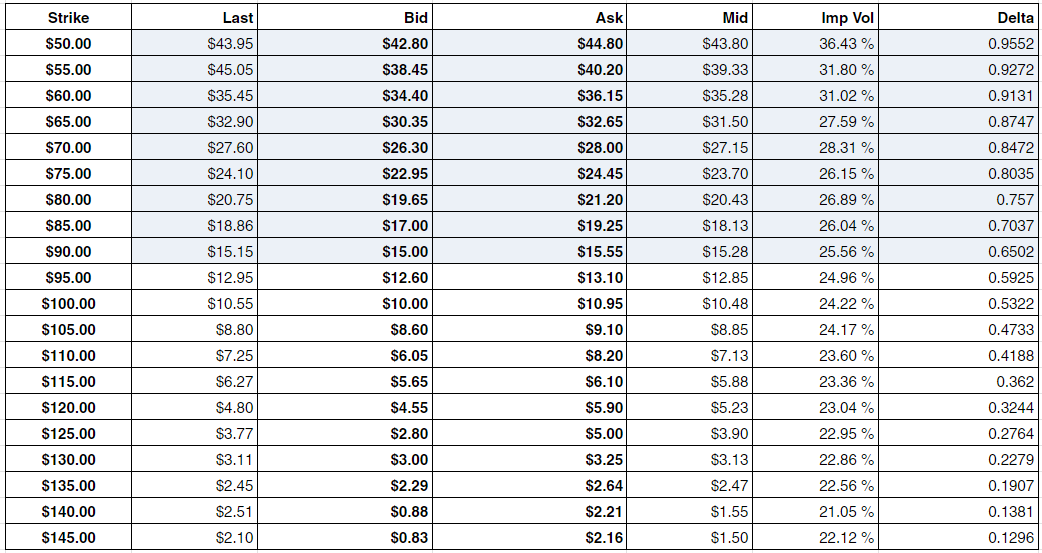

The Options

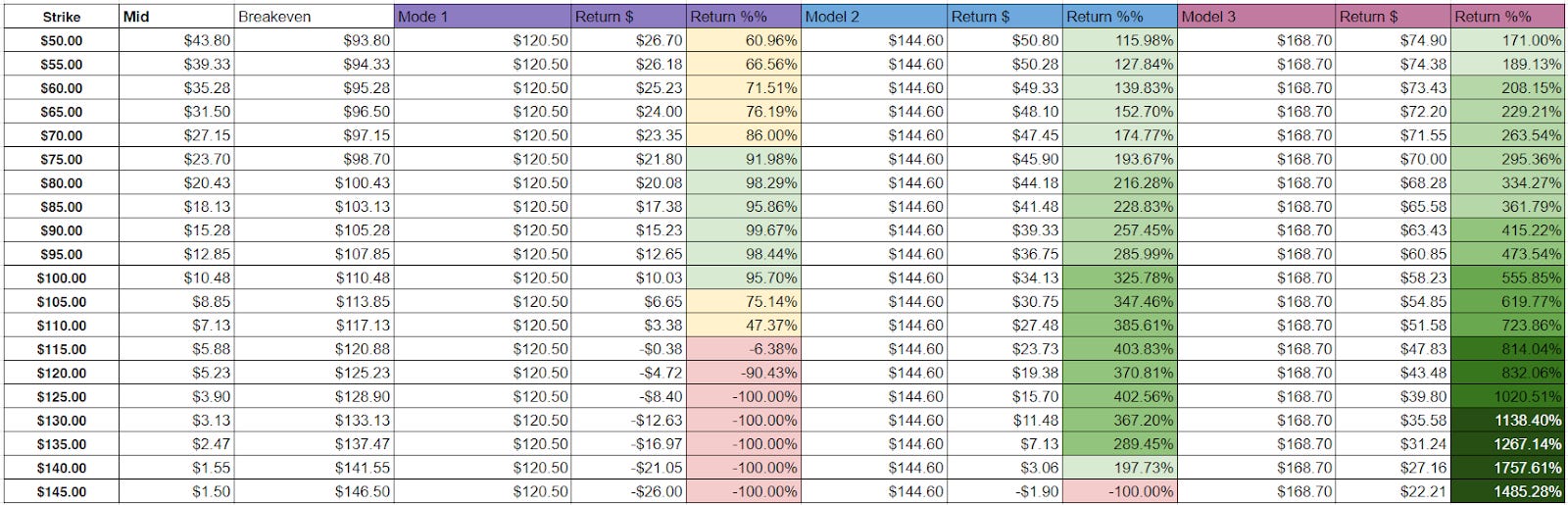

The Potential

The big chart is above! Look at that beauty! What you can see is that, based on the consensus earnings, the PE valuation is likely to drive most of the outcomes. With a PE ratio of less than today’s 25.7, going down to 25, the LEAPs have 6 strikes that roughly double. With any expansion at all, you can observe that the returns increase dramatically. Considering the potential upside increases, and what I think is most likely, I am going to add the $100 strike to the scoreboard. This is a time when many choices cater to different risk profiles – it is truly a 'choose your own adventure.' Hope this gives you some ideas.

Regards,

S.