Mastercard (MA) - Exploring our Options

I see you 2025

Mastercard – MA

Background

From them https://www.mastercard.us/en-us/vision/who-we-are.html:

“We work to connect and power an inclusive digital economy that benefits everyone, everywhere by making transactions safe, simple, smart and accessible. Using secure data and networks, partnerships and passion, our innovations and solutions help individuals, financial institutions, governments and businesses realize their greatest potential. Our decency quotient, or DQ, drives our culture and everything we do inside and outside of our company.”

From me:

All those buzzwords boild down to this; they process payments. Mastercard is the Coke to Visa’s Pepsi, another payment processing corporation. Though maybe Visa is Coke and Mastercard is Pepsi. They are both huge and well known, but the internet tells me they are both #2 worldwide. Perhaps the way to the top in finance is being humble?

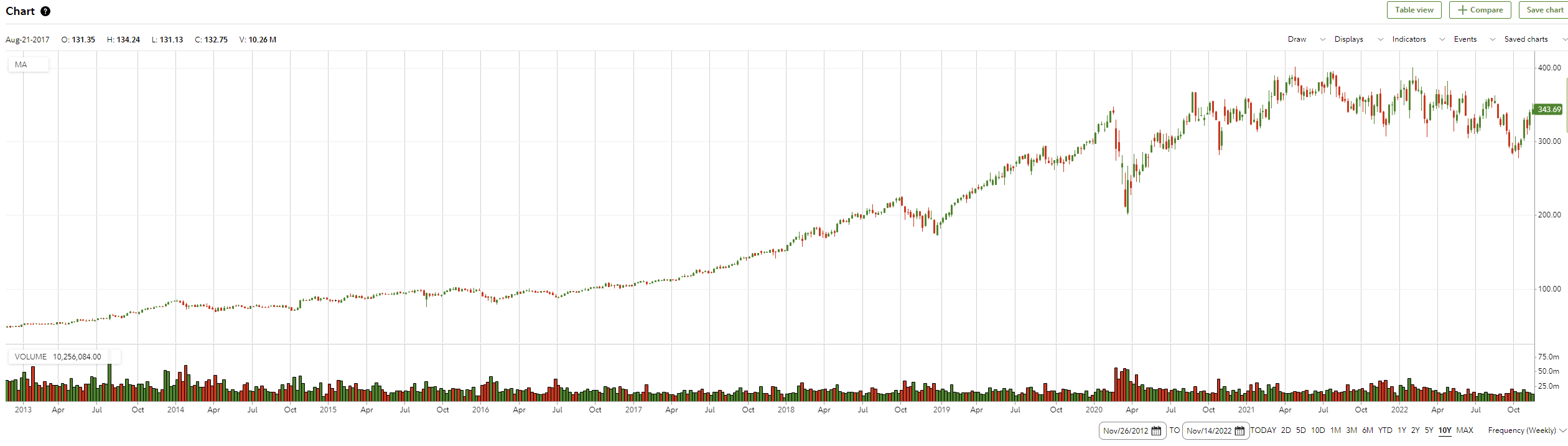

Graph

Valuations

Trading at $343.69 as of Friday 11/18/2022 Mastercard has done well over the past ten years with shares going from ~$46 to ~343. Without dividends, turning each dollar back in 2012 into $7.5 today. Not bad. Where do things stand now? Mastercard’s TTM PE is 34.3 with earnings of $10.01 per share. Over the past five years the average PE has been 41.5. Past 8 years the valuation band has been 24.2 PE at the bottom to an eye watering 55.4 PE at the top. In the past 8 years things have been anywhere from the high twenties to the low 40s, so there is some room for interpretation on what to use as a future value.

So, what does that mean?

Mastercard is also covered by a ton of analysts with 33 covering it distilling down to an estimate for 12/31/23’s yearend to be $12.18 for EPS. They also expect the 3–5-year future growth rate to be an impressive 21%. Considering the past 5 years have averaged a growth rate of 19% through a global pandemic, I would think that is reasonable. The highest anyone has for new years eve 2023 is a cool $13 per share and the lowest is a nearly sideways $10.71. To get my projections for the year ending on 12/31/24 applied 21% growth to the analysts’ numbers. That will give us the low of $12.96, a high of $15.73 and the distilled coming out to $14.74. If the fed crushes inflation without hurting the economy too bad we may see the 5 year average come back for PE, if things go poorly growth may not happen and the valuation could even go down.

Projections

Using the numbers above for EPS and the different PE values Mastercard has seen over the year I have generated the table below. I will be focusing on the consensus number and the range between our current PE and the 5-year average. The rest of the values are here to show what extreme cases could look like

Options

What do January 2025 Call options cost these days? As of Close of business Friday 11/18/22:

For most of these the last was outside of the Bid/ask range so I am using the mid as my number for the math going forward.

Outcomes

The Table below shows the outcomes of the different strike prices based on my projected Mastercard stock price of $505-$611 come January of 2025:

This seems a little too rosy to me. In this case I am going to use the $12.96 Eps off Friday’s PE of 34.3 as a secondary measure. This adds 2 columns for January of 2025 with a $444.53 projected stock price.

With those columns added to the table we seem to have more paths to a good outcome if we stick closer to today’s stock price for our strike.

There it is. My projections. For the scoreboard I am going to go with the $310 strike. 20% over two years is fine for a worst-case scenario and for what I view as more likely ranges, the return could still be something special (double to triple). The only downside to this in real life is that a $93.90 option costs nearly $10,000… Luckily this is merely a newsletter to give you ideas. Hope this helps. Please share with anyone you think will find this interesting.

Regards,

S.

Scoreboard: