Kimberly Clark, Sleeping Giant

Kimberly Clark, Sleeping Giant

Leaving a Paper Trail on This One

Our next option on the year-end list spotlights Kimberly-Clark (KMB), a company that may not be a household name, but undoubtedly plays a significant role in your daily life. Specializing in the manufacturing of consumer goods, particularly those made from paper, Kimberly-Clark boasts ownership of well-known brands such as Andrex, Cottonelle, Depend, Huggies, Kleenex, Poise, Scott, U by Kotex, and Wypall.

With a workforce of 45,000 employees, Kimberly-Clark is a substantial Large-cap company, commanding a market value of $40.5 billion. Undeniably a major player in its industry, the company is also an esteemed member of the exclusive dividend aristocrat club. This elite group comprises companies that have maintained a position in the S&P 500 for 25 consecutive years while consistently increasing dividends annually. This track record has led to historical premium valuations for these companies, making them prized assets in numerous blue-chip portfolios.

A 10-Year Walk Down Memory Lane

Over the past decade, Kimberly-Clark (KMB) hasn't delivered an exceptionally impressive performance, with only a modest 20% gain (inclusive of dividends). Earnings from that period don't deviate significantly from the current figures. However, contrary to the historical trend of relatively stagnant growth, there are optimistic predictions for substantial gains in the next two years.

As of today, each $120 share corresponds to $5.20 in earnings, resulting in a Trailing Twelve Months (TTM) Price-to-Earnings (PE) ratio of 23.1. This stands close to the 5-year average PE ratio of 23.3, indicating a relatively stable valuation in comparison to the recent past.

Projecting Forward

KMB is anticipated to announce full-year earnings in January, with expectations of boosting earnings per share (EPS) to $6.59. Looking ahead, 2024 and 2025 are projected to bring further earnings growth, with an estimated 3-5 year EPS growth rate of 9.3%. Given our interest in acquiring LEAPs expiring in January 2026, it is crucial to focus on the 2025 estimates.

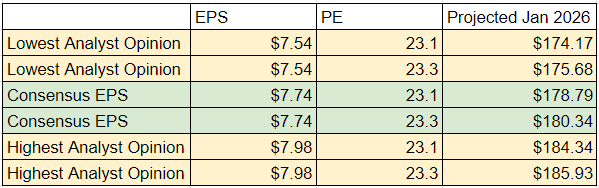

To arrive at these estimates, we rely on the 2024 projections provided by 17 analysts, ranging from a low of $6.90 to a high of $7.30. By applying the expected 9.3% growth, we can extrapolate these figures, resulting in a low estimate of $7.54, a consensus estimate of $7.74, and a high estimate of $7.98. When incorporating these values into my standard chart alongside the two PEs mentioned earlier, the outlook is as follows: [chart details].

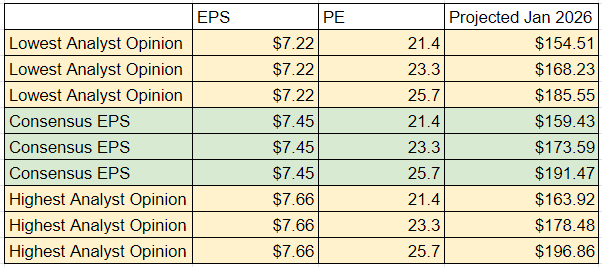

The initial band appears relatively narrow, lacking the breadth to encompass the diverse range of outcomes I wish to explore. To achieve a more comprehensive perspective, I'll rely on the analysts' numbers for 2025, acknowledging the limited sample size of 5 analysts, thus taking their projections with a grain of salt. According to their estimates, the expected EPS for 2025 is $7.45, with a high of $7.66 and a low of $7.22.

To provide a more well-rounded picture, I'll consider the lowest Price-to-Earnings (PE) ratio from the past 10 years (21.4) and the highest (25.7). This broader approach yields the following outcomes: [details of the outcomes].

Here we have a bigger range with a lower floor and a similar ceiling. That seems prudent given the timeframe we are looking at.

The Options

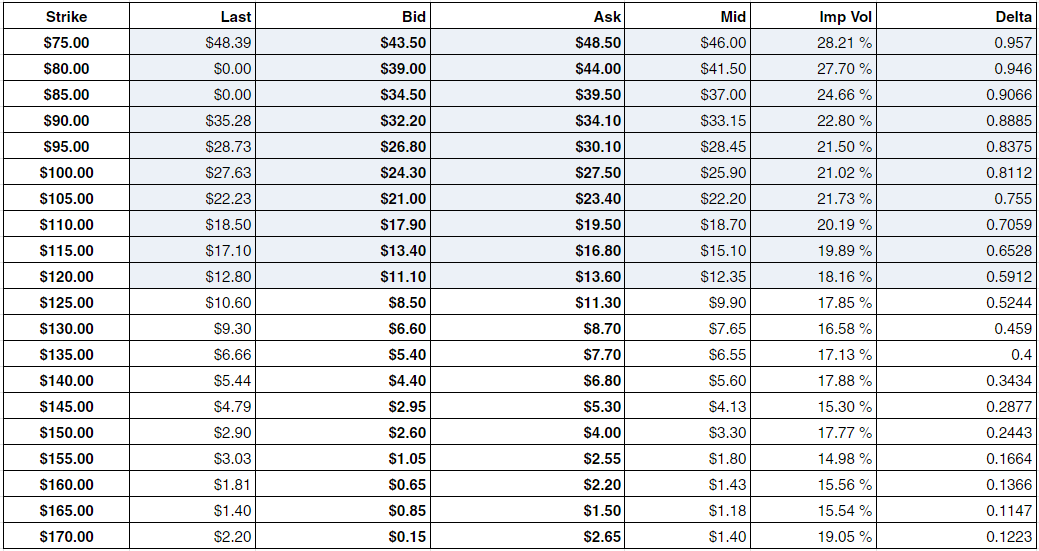

Now that we have our ballpark of what the underlying stock may trade at, what do our options look like?

Pretty standard fare. Quite cheap for a stock expecting some growth with potential for PE expansion. How would those numbers against the projected stock prices look? What returns could be seen?

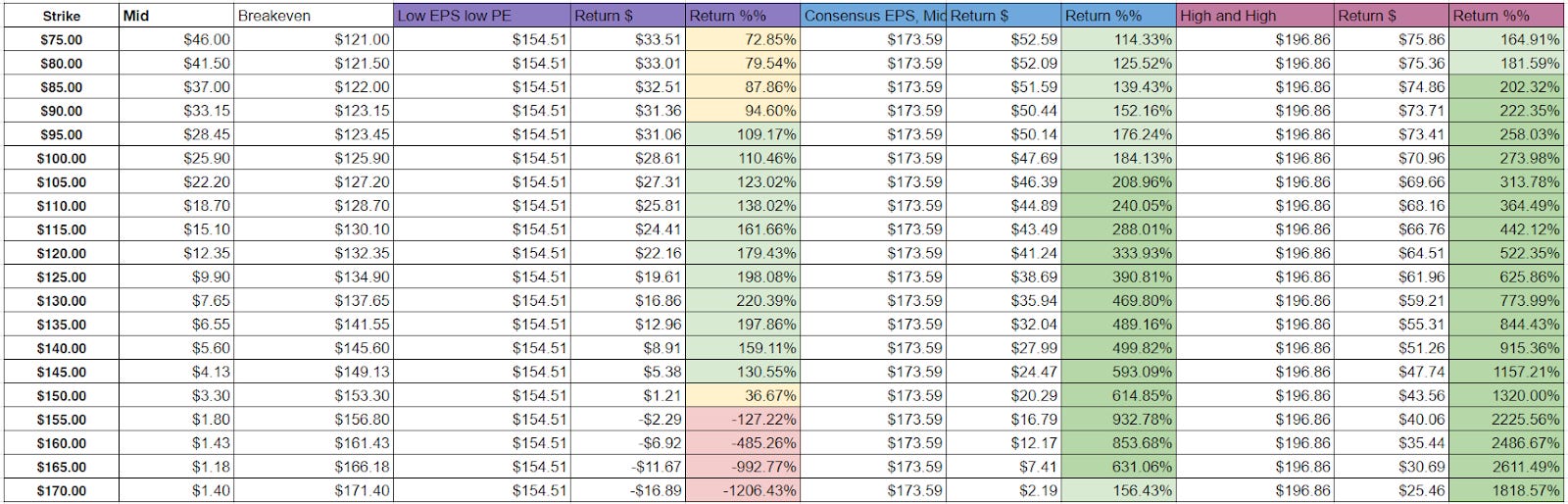

The extensive chart illustrates a range of outcomes in our contingency plans, covering scenarios from the worst-case to more optimistic ones. Notably, buying near the strike presents a nearly triple return, offering various options for different return profiles. The returns for less likely but higher outcomes appear exceptionally lucrative, though we should approach them with caution given their speculative nature.

I propose adding the $130 strike option to our scoreboard, as it holds the potential for significant gains. Additionally, I'll introduce the $155 strike, a departure from my usual approach. This serves as a speculative move, acknowledging the possibility of a total loss, while going for the upside. The break-even point is close to our floor estimate, providing potential exit points before expiration if needed. If the investment pans out, the returns could be extraordinary.

Stay tuned for more updates this week! I intend to maintain this brisk pace as I realign my portfolio for the year, with a likely slowdown in activity thereafter. Happy investing!

Regards,

S.