Johnson and Johnson

| Video clips by quotes | 686f6578 | 紗")

Johnson and Johnson, here we are! As mentioned in my previous post, it is our next write-up. A long-term staple of any blue-chip portfolio, JnJ is a dividend aristocrat. It tends to grow its earnings in the single-digit percentage-wise, and with a 3% dividend yield, it can often get investors a respectable 8-12% return over the long haul. This past summer, it divested the consumer portion of its business into a new company, “Kenvue.” This leaves behind the faster-growing medical side of things and was supposed to increase the company’s ability to grow. Instead, JNJ sits near its 52-week low, at a price seen before COVID started 4 years ago. They’ve gone up and down, and here we are. They are a prime value play for Rolling Thunder, and you will see why below.

Where we are:

Here you see what I mentioned above; things have gone sideways over the past 5 years. 5% over 5 years isn’t something to write home about. If you bought the underlying stock, you would have collected another 10-15% in dividends and could have opted into Kenvue if you were interested. This still is pretty lackluster. The end of 2020 saw JNJ earning $7.93 for the year (including the spinoff Kenvue items) and it finished 2023 at $9.92. While earnings grew by $1.99 (25.1%), the stock price did not, nor did its valuation. Revenue during this time grew by about 1% per year. Somewhat like Pfizer, JNJ had its revenue balloon from COVID products, and that has now largely evaporated.

Looking Forward:

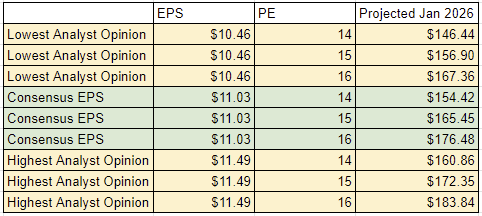

This year JNJ gave guidance of $10.55-$10.75 for earnings per share, and most analysts are expecting 2025 to come in between $10.46 and $11.49 with the consensus being $11.03. Any option we purchase for January of 2026 will not include the last quarter of 2025, so things may be a smidge lower than that. Post-financial crisis before COVID, JnJ typically traded between a P/E of 14 and 16 with some periods of it trading in the higher teens. This seems pretty reasonable to me, and I think the play here is to value it as a worst-case P/E of 14, and we would be hoping for a sale at a period in the higher teens. What could this look like based on the earnings projections? We will do a tight band of 14, 15, and 16 for P/E. There is a chance the P/E expands further, but we can’t count on that.

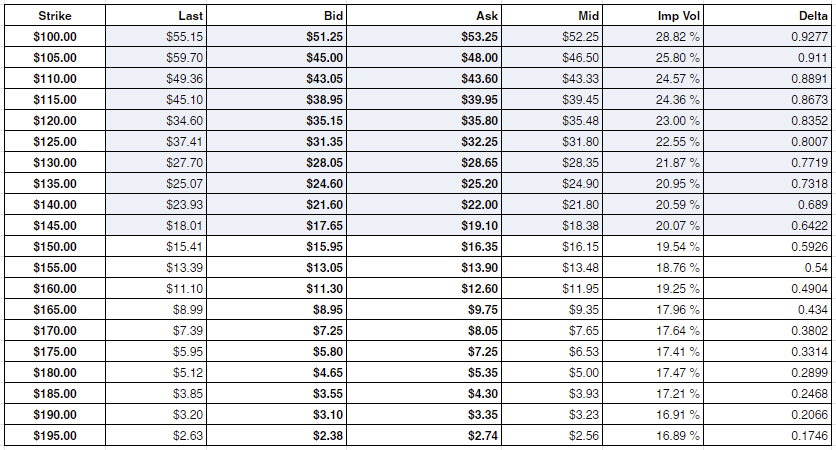

That would give us these values once year-end earnings were reported. Now that will happen after the LEAPs expire so these aren’t perfect numbers, but if JNJ looks like it is going to hit its target, it is likely these values are close enough for our modeling. The current options look like this:

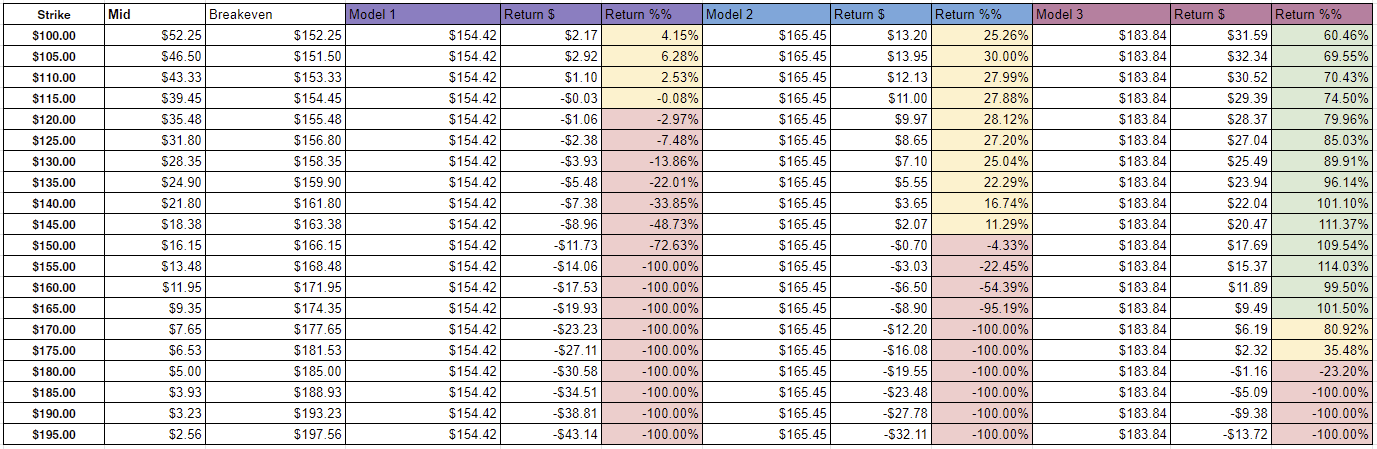

Taking those together we can look at what options could give what returns in the next table. I am going to use the P/E of 14 with the consensus earnings per share as our worst case. If JNJ is guiding for $10.55-10.75 this year, I don’t expect we will see next year any lower than that. I will use the 15 P/E on the consensus $11.03, and if things go best case, I imagine the P/E will expand to 16. This means we will look at the stock trading at $154.42, $165.45, and $183.84.

This winds up looking like a riskier proposition. For the worst-case model, most options are essentially a wipeout. If the P/E remains steady and things go as planned, you aren’t much better off buying the options than just buying the underlying and collecting the ~20% return that would take place via returns and dividends. To hit a double, we would need JNJ to hit the high end of its earnings expectations AND have a P/E expansion. There have been stretches of time longer than what we are looking at with the valuation staying right around a P/E of 15. Of course, if the world keeps getting crazier, this blue chip may get bid up, and there are some paths for a P/E of 18/19 to materialize, but that is hard to count on. If I were to go out and buy an option today, I would likely pick the $155 strike as I think it gives the best upside for the least downside, but it isn’t the slam dunk I look for. I could see a world where they settle the Talc lawsuit, and perhaps mood shifts and they trade at an 18-20 P/E again, but if that is the only way to green, I would rather go with something else.

This is a time where I have taken a stock from a screen and run it down. I read its reports and modeled its future and just don’t see that great of a path. There are paths where this could work out, but too many of them don’t. I would rather put my eggs in the basket of some other recent calls like Starbucks.

Hope this helps,

S.