How and When?

I bet you’ve been asking yourself how I find my targets and when I write them up. I plan to use this post to go over that. When it comes to finding my LEAP targets, I approach things through one of two lenses. These will hardly shock anyone who is into investing, but they are Value and Growth. The Value lens can be exceptionally lucrative when done right, as the beaten down can come roaring back to life in a way that is hard to imagine. This can make a well-constructed option trade go 3x pretty easily. The Growth lens is somewhat the opposite; it is a game of who is doing well and will continue to do so. If each dollar made is worth a 30-40x multiple, then making a dollar more moves things considerably. Some things remain the same for both approaches. For instance, I want to know and understand what the company does and believe in its ability to continue onward. Also, I typically stay in the S&P 500, part of this is to the point before (I’ll know them) but also, these companies are more likely to have LEAPs. I also have a list of companies that I am a big fan of. These companies may not always fit into either bucket and be things to make LEAPs on, but they are the ones I am hoping become candidates.

Value and an Example

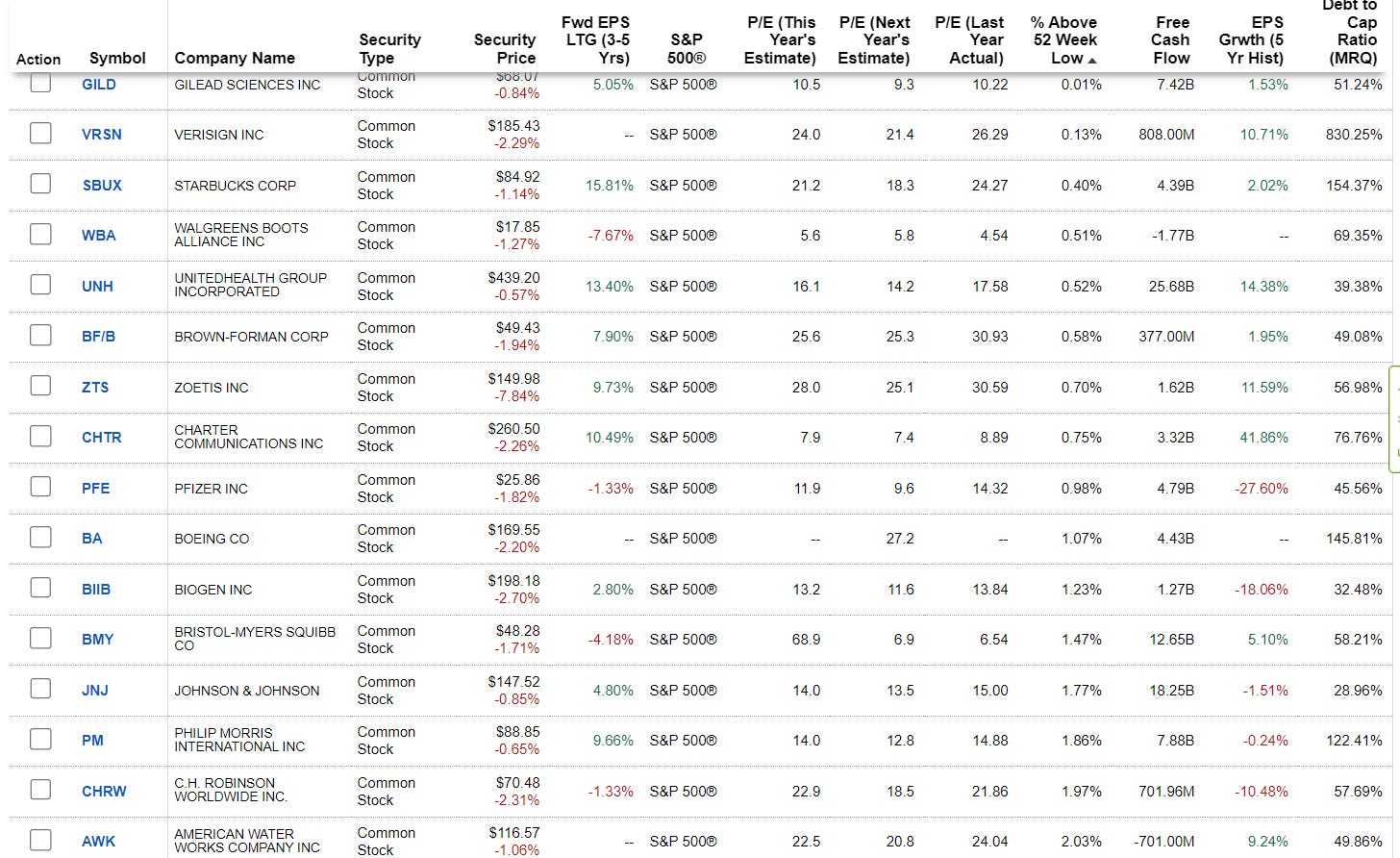

Value can be found a few different ways, but one easy way to find the most beaten-down stocks is in a simple screener on the S&P 500 for who is near a 52-week low. Sometimes the best value companies are mid/small caps but they often lack LEAPs, and sometimes the most undervalued company isn’t one that is languishing at the 52 week low, but one that is treading water somewhat. Regardless of all that, this is a way to start. Say I run a screen like that on the S&P 500 as of this weekend, the bottom of the barrel is:

You may recognize some of these companies; I know I sure do! I have written about some, and my top target right now remains Starbucks, but since we already know I like them and have a post, let’s skip them. So now what? These companies are in the shitter. Which ones are worth buying? What can be made into a LEAP candidate?

Different industries use debt differently, so it isn’t an apples-to-apples thing, but you may look at the board and see a company that is very in debt, in this case, Verisign. I don’t know what they do, which is another knock, but sometimes a company’s corporate name is different than the brands you know and love. When I go to read up on them I see that I do not in fact know them or understand them I also see a -$16 per share of book value. I take them off the list. For me, that is an easy one to not look at.

Another thing that can’t be seen from this screen (at least as far as I have been able to tell) is does the company have LEAPs? For Rolling Thunder, we really do not need to waste time with companies that don’t trade long options. BF/B Brown-Forman is a company I am very familiar with. They make booze, and they make it well. They are a great blue-chip stock, but when I go to their options page, they don’t do LEAPs. So while it may be a good pickup for your portfolio, it won’t do for me as a Rolling Thunder post.

One way that any stock but especially value stocks can offer big returns is when they have a PE expansion, and conversely, a contraction can really bite you. If things stay mostly stable, that is not a bad thing for predictions, but isn’t exactly good either. How can you determine what may happen? If cash flow has gone negative, a company may have trouble paying its dividend. In the case of Walgreens WBA, this recently happened. Not only did this indicate things were going poorly, but it also knocked them off the esteemed Dividend Aristocrats list. That Aristocrats are companies that have paid and raised a dividend for 25 years straight or longer. With a track record like that, they tend to keep a higher earnings multiple as they are considered trusted and reliable blue-chip stocks. So while that makes a company on that list worth more (typically) it means pain when one must leave (like Walgreens). This doesn’t mean Walgreens is a bad play oddly, as it needed to preserve cash and it is now trading at a very low price, but they looked kind of similar 6-8 months ago and are down 50% since then. Where is the bottom?

Back to the Dividend Aristocrats, they are a pretty good place to cross-reference the cellar dwellers for candidates. I used https://www.simplysafedividends.com/world-of-dividends/posts/6-2024-dividend-aristocrats-list-all-67-our-top-5-picks for my current list. They have a download for the Excel list and note what dividends they consider to be safe. Now my bottom of the barrel screen had more stocks in it, but of those in my screenshot, only 3 are on that list, BF/B, JNJ, and CHRW. According to simplysafedividends CHRW has a borderline safe dividend, implying some risk. I am not super familiar with that company, but JNJ is a household name. They are well capitalized, with a projected 5% growth, and a fair PE multiple for the growth expected. They offer LEAPs at a cheap IV of 19%. At a glance, there are a lot of paths to break even, and if there is any good news and the PE expands towards its historical high teen/ low 20 multiple, that could be great. As it spun off its slower-growing consumer business to be Kenvue, it also has the potential to trade at a new higher valuation that was as well. It was expected the split would, in fact, increase JNJ's proper growth. This has all of the right indications to be a good candidate for a LEAP trade. This would be the point where I would start my deep dive, read recent filings, and project values for the stock to trade at come January 2026. Should everything line up, I would then create a post. In this case, I expect you will see a post on it soon!

Growth and an Example

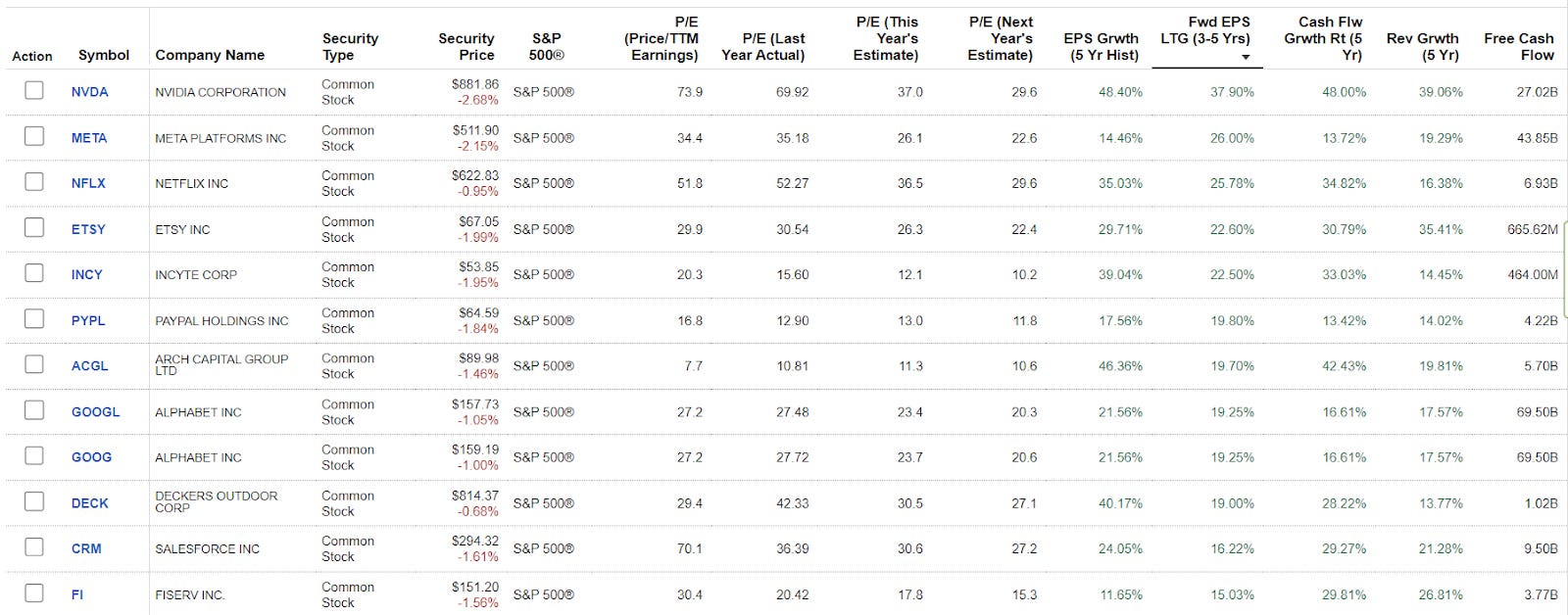

Now the other side of the coin, growth. This is the space where the highs are higher, but the lows can certainly be lower. Pick any top-tier growth company from the past decade, and you will see many many times where what was the all-time high is quickly left in the dust by an even higher new high. They also have some risks when growth slows of the company value going down rapidly as well. The options tend to be a bit pricier with high growth, but when each new dollar earned is adding $30 or more to the share price, these options can also play out nicely. Similar to the value section, a screener is a place to start for ideas. I tend to stick with the S&P 500 like before for the same reason - easier to find stocks that have LEAPs, and I am more likely to know the company and what they do. I like to look at companies that are expected to grow earnings at a high rate 15% and above over the next 3-5 years and narrow it down by who has done strong growth in the past 5 years through the pandemic and inflation. I capped next year's PE at 30, because with the forward growth of most of these companies, I wouldn’t pay much more than that for them. That list looks something like:

Unsurprisingly, there is a lot of tech and household names on there. You also see a familiar value play in PayPal, as it is poised for growth but isn’t appreciating much. Google is another you here have seen me write up. Both came into my sights as combination value+growth plays, but now I would say Google is more of a pure growth stock. The others we will need to sort through.

Once again there is the chore of checking which of those companies offer LEAPs, most do but some do not. These companies are largely the darlings of the investor world right now, and most are near 52-week highs. While that can be daunting, many times these are the companies that leave their all-time highs in the dust. For instance, NVIDIA, it has been on quite a tear and is ~10% below its 52-week high. Even though it has more than tripled in the past 12 months, it is the primary chipmaker for the AI boom and has every reason to continue to do well. So while this is today’s peak of the mountain, it may be a mere foothill in a few years. The same can be said for many of these companies to some degree. Growth is scary and exciting that way!

Of those 12 stocks listed, 2 are Google and I have covered that already, and one is PayPal, also on our list. Incyte, Deckers, and Arch Capital don’t offer LEAPs so they can come off the list for Rolling Thunder. I do really like Incyte as a company and think it is a worthy investment in general, just it is impossible for this strategy. This leaves us with: Etsy, Netflix, Meta, Salesforce, Fiserv, and NVIDIA. Mostly tech companies here and mostly things I know of offhand except Fiserv. I made some value plays on Meta and Netflix when tech was depressed a year and a half ago and sold out too early, so my mind has them anchored to a price that will likely never be seen again. I need to shed that from my mind. Today and the future from here is what matters.

So how do I narrow it down from here? I ask questions like “Do I think they can grow as expected?” “What could happen that would derail said growth?” “What companies do I believe in the most?” “What is the debt situation? What liabilities and assets may factor in?” “How much would a LEAP cost?” “How much cash is on hand?” When I finish those questions, maybe a company isn’t a good fit. It also may be time with just 6 companies to look at to review recent guidance, read company filings, and dive deep. A screen or quick metric may not help much. In this case though, NVIDIA is probably the last one I will look at. Perhaps it could be the best investment, but each LEAP would cost $30,000 which is a bit prohibitive for most people. Etsy, Meta, and Netflix would all be running the $15-20k themselves, so also not cheap. If I am writing these up for others to consider as investments, I would like them to be at least somewhat accessible. Fiserv and Salesforce are in the $2-7k range which is more approachable for most people. That is all to say I wouldn’t rule any of these companies out immediately, but I will start with Fiserv and Salesforce. I expect you will see a post or two about them soon as well!

Conclusion

So that is how I approach things. There is a Value and a Growth lens to my method. Each has a place and the things I have shared typically fall into one of those buckets (I skew value). Keep your eyes peeled this week for posts on JNJ, Salesforce, and Fiserv, they are likely coming! Until then I hope you enjoy your weekend.

Regards,

S. Andrew