HERSHEY'S 2026 LEAPS

Hershey!

*How can you not love a creepy AI generated chocolate bar?! Look at that smile!

What could be more timeless than a Hershey bar? Embraced by countless generations of Americans, this company has been crafting delectable treats for over a century. Evolving from the iconic Milk Chocolate Bar, they've ventured into a diverse array of confections, established an amusement park, and acquired various other assets. A darling of dividend investors, Hershey is often considered a long-term hold, commanding a premium due to its consistent earnings.

However, the company is currently navigating challenges, reflected in a stock price lower than its historical norm. While the pandemic led to increased sweet consumption, the post-Covid era sees uncertainties for the confectionery industry. Despite these headwinds, I remain optimistic about Hershey's prospects and believe it's worth a closer look. Let's delve into the details!

Past Performance

Over the last decade, Hershey has seen its stock value climb from just under $100 per share to the current $192 per share. While this reflects a relatively modest 92% return, it lags behind the overall market, which witnessed a 250% surge during the same period. It's worth noting that Hershey does provide a dividend, enhancing its overall appeal. Typically, the company yields a 2% dividend, compared to the index's 1.5%, so the difference in returns is not significantly large based on the above comparison.

However, in the past year, Hershey has experienced a notable downturn. This recent decline presents an opportunity that we aim to leverage.

Earnings and Potential Earnings

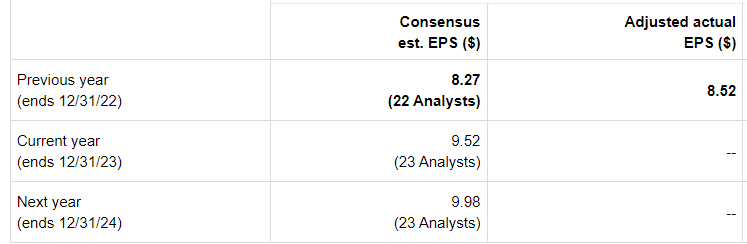

The chart above illustrates Hershey's performance in 2022, its projected closing figure for 2023, and the anticipated expectations for 2024. Considering our focus on 2026 options, we'll also attempt to project potential outcomes for 2025. Notably, Hershey has consistently surpassed earnings estimates for at least the past eight quarters (I haven't examined further back), making it reasonable to anticipate a $9.52 per share for 2023.

As for 2024, predictions from 23 analysts suggest an earnings per share (EPS) just under $10, specifically $9.98 ($9.50 as the low estimate and $10.30 as the high estimate). Looking further into the future, analysts anticipate a growth rate of 8.3% over the next 3-5 years. Armed with this insight, we can estimate a $10.80 EPS for 2025 ($10.29 as the low estimate and $11.15 as the high estimate), simply by applying the projected 8.3% growth from 2024.

In cross-referencing with other sources on the web, I found estimates from 6 analysts for 2025, and while slightly more conservative, they align closely, deviating lower by about $0.30 on all figures.

The Future!

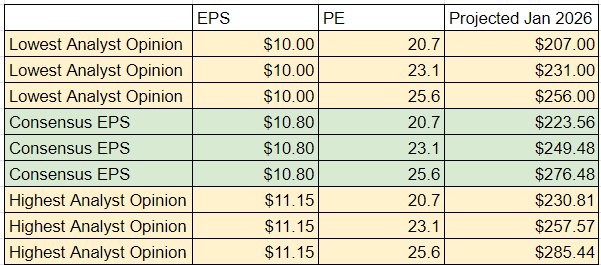

Now, having established a narrow range for potential earnings, let's delve into what the company might be worth in two years if it achieves the projected earnings. Over recent years, the stock has exhibited varying price-to-earnings (PE) ratios, ranging from the 20s to as low as 17.5 in 2018 and as high as nearly 30 recently. Currently, it stands at 20.7, with a 5-year average of 25.6.

Considering the economic landscape's anticipated improvement in the coming year, particularly if inflation remains subdued and interest rates are cut, most stocks are expected to witness increased valuations. Using the 25.6 PE ratio doesn't seem unreasonable, especially given the recent PE of 30. On the conservative end, today's 20.7 is a plausible figure, as I don't foresee a significant dip for an extended period. The 5-year average of 25.6 serves as a robust high, and in this scenario, opting for the middle ground with 23.1 seems prudent.

So, with PE ratios of 20.7, 23.1, and 25.6, and considering a $10.80 EPS ($10.29 low and $11.15 high), we can project potential stock values:

The Consensus EPS estimate provides a trading range of $217 to $276, indicating where the stock is likely to trade. Any fluctuations in earnings can potentially shift this window slightly. Despite a sense that this range feels low, influenced perhaps by an anchoring effect from the stock's higher value this spring, it's essential to consider this objective estimate. Now, let's move on to the discussion of options!

The Options

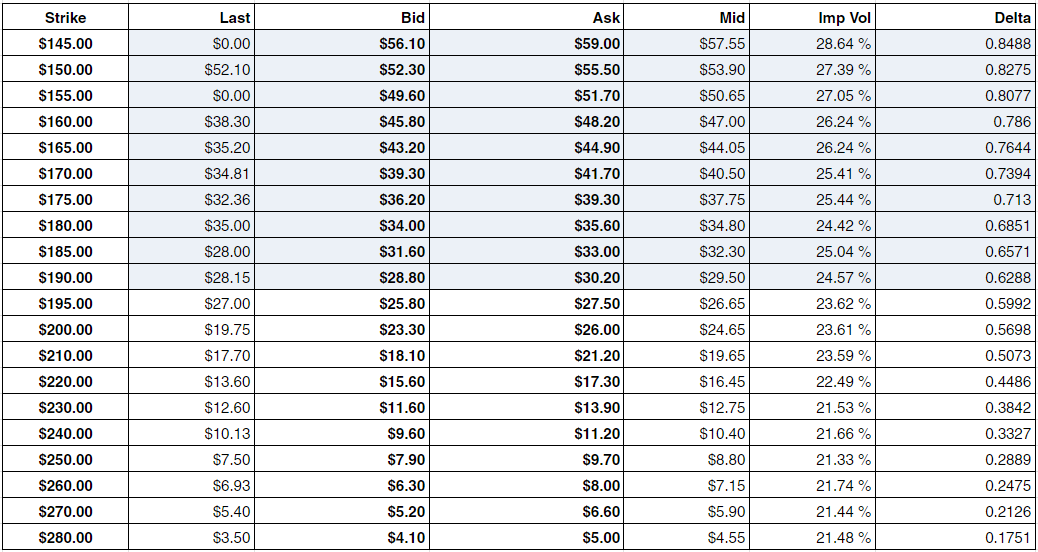

For January 2026, the options are represented in the table below. Please note that these values were captured near the end of trading yesterday, and there might have been slight movements since then.

The IV is in the low 20s, which aligns with my preference in the Rolling Thunder world. Keep in mind that, as we move further from the money (current stock price), the volume tends to be lower, impacting the accuracy of the mid option prices. Now, onto the crucial part—let's apply the anticipated stock values to these options and examine the potential returns. A quick warning for those sensitive to large tables: look away!

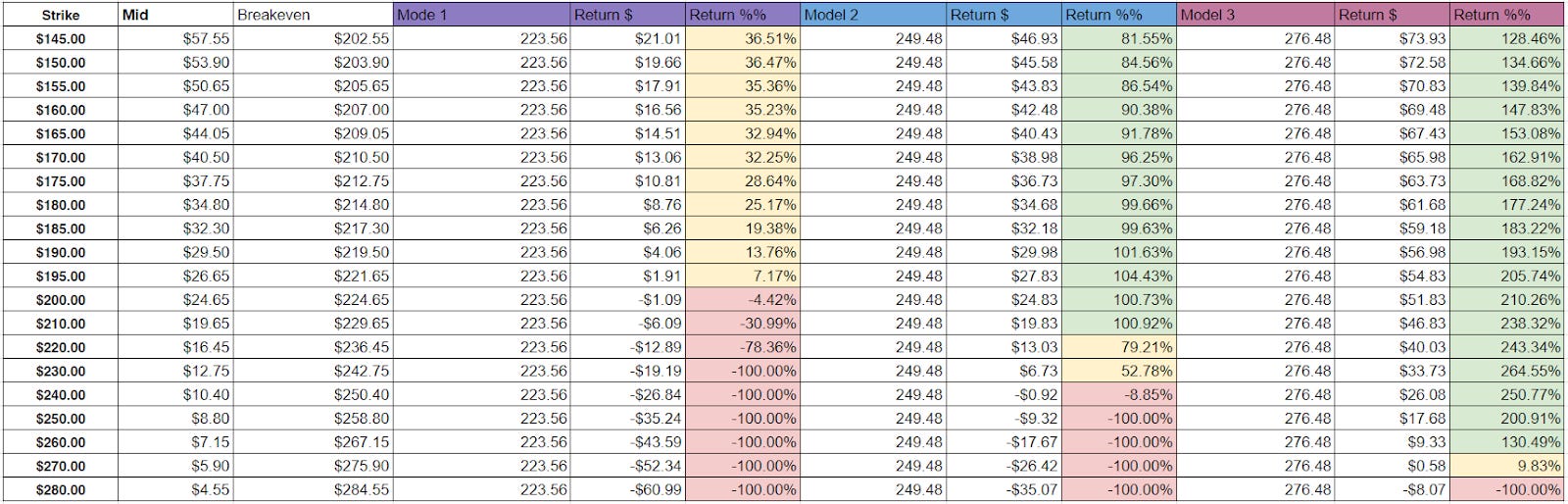

This table provides valuable insights. In our conservative model, where the stock hovers around $223, certain options offer low returns and some barely break even. Out-of-the-money options would likely end up worthless in this scenario. Moving to a more optimistic scenario with a PE expansion to 23.1, numerous options appear favorable, tapering off around the $220 strike. In the best-case model, where the stock trades near $276, most strikes yield at least double returns, with some even tripling or better.

Individual risk tolerance varies, but personally, I find the $195 strike appealing. In the worst-case scenario, it essentially breaks even at 7%, while in more favorable situations, it presents the opportunity for a double or triple return. Therefore, I'm inclined to add the $195 strike to the board!

Even if this trade isn't for you, I trust I've provided some valuable considerations. One aspect I don't always emphasize but is consistently true is this: if you're fond of the stock and its value, you always have the OPTION (pun intended) to buy the underlying asset instead of the option. In the scenarios discussed earlier, holding the stock could yield returns ranging from ~10% to ~43% over two years, which is good for a historically reliable blue-chip stock. While Rolling Thunder aims for a double or triple by leveraging the stock's consistency through LEAPs, other strategies can also prove effective! Happy investing!

Regards,

S.