Google Revisited

What’s happened?

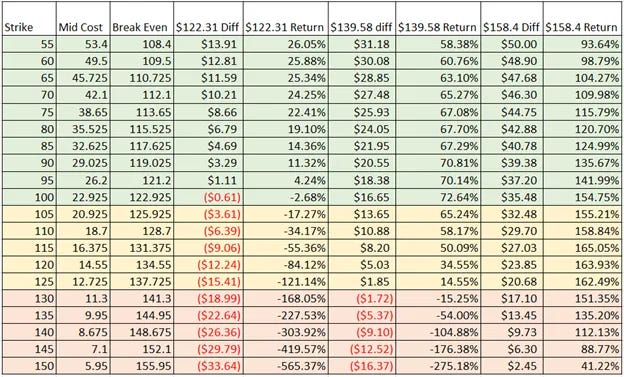

It has been a bit over a year since I first wrote about Options on GOOGL. At that time, Google had lost value from its 2021 high of ~$150 and was sitting at just about $100 per share. As of March 2024, it is back to that high point and sits at $150.93. At that time, analysts expected earnings growth at a lower 10.4% for the coming years. With the layoffs and some other changes, Google now appears to be back on track. The forward EPS estimates are 19.25%, and it has also been growing faster than expected. With the growth expectations from a year ago, I modeled the June 2025 stock price using a TTM (Trailing Twelve Months) earnings of $6.02. Google improved so quickly it ended up earning $5.74 for 2023 instead of the predicted $5.19. It is now expected to earn $6.81 this year and $7.85 in 2025, with that 19.25% growth as the placeholder thereafter. This adjustment changes our expectations somewhat. We had landed on the June 2025 $100 Strike at $22.92 for the original piece. Those options are now worth ~$58.10 as of market close Thursday, representing a return of 153.5% in just over a year, nearly hitting our best-case outcome in half the time. Our chart from 2/2/23 is referenced below.

We were looking for a 70-150% return with the potential for further upside. We sit halfway there and at that 150% mark with what looks like plenty more return on the table.

Now What?

Well great, that is a big win. What’s not to like? Decisions. That’s what. What do we do now? Do we let this investment ride for another 15 months to potentially capture further gains, or sell now and secure a big win? My original analysis had Google's stock potentially reaching around $158 a share. The high end estimate from my original piece had Google trading around $158 a share, so if the thesis that got us there is the same, we likely should move on, but if the situation has changed then so should our expectations. The general sentiment on Google has notably changed, with the forward Earnings Per Share (EPS) growth estimates nearly doubling from 10.4% to 19.25% since our initial analysis a year ago. This adjustment was somewhat anticipated, given the scale of layoffs. As previously mentioned, the new earnings estimate for this year stands at $6.81. Projecting two more quarters of growth gives us a Trailing Twelve Months (TTM) earnings of approximately $7.42 by June 2025. By comparing the lowest and highest analyst estimates, we can gauge our worst and best-case scenarios against earnings of $6.52 and $8.28, respectively.

Another critical factor in calculating the stock's value is the Price to Earnings (PE) ratio. A year ago, it hovered around 20.3, with a five-year average of 23. Currently, it's trading at a PE ratio of 26, against a five-year average of 23.4. For much of it’s history, the stock has traded between 25 and 33 times earnings. This suggests there's still potential for expansion if the good news continues. However, for our modeling, we'll use the more conservative five-year average PE of 23.4 and the current PE of 26. This analysis leads us to:

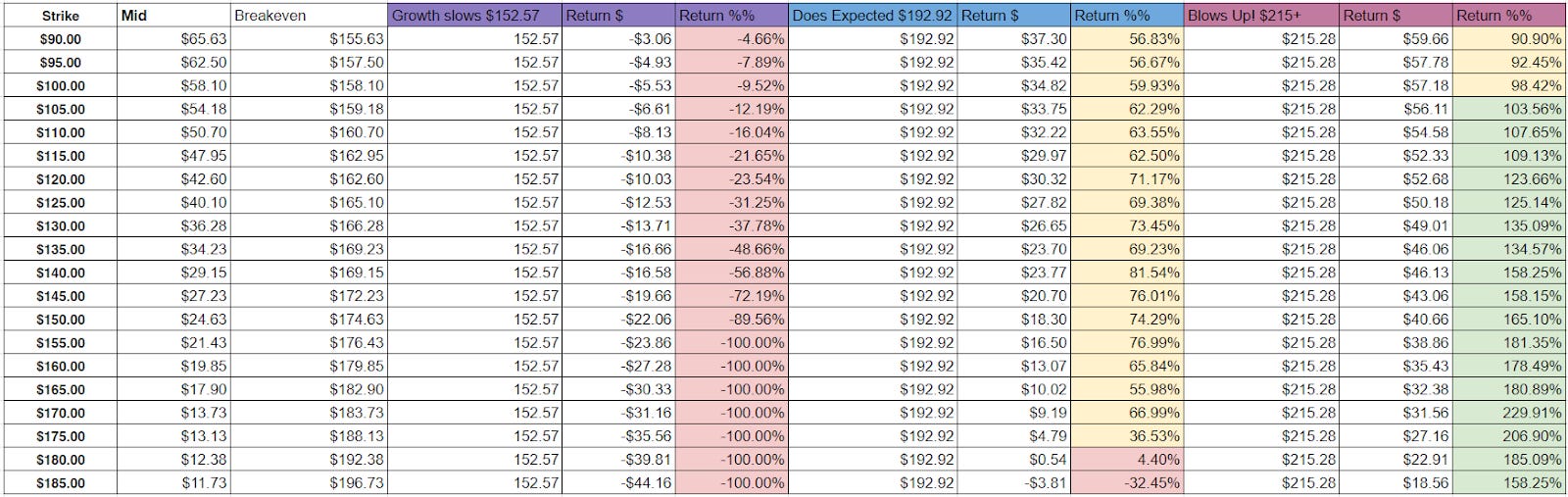

I personally find it quite unlikely that Google will achieve the anticipated earnings growth rate while experiencing a contraction in its PE ratio. Therefore, if we see approximately $7.4 in TTM earnings next spring, the stock will probably still trade at 26 times earnings. Should growth falter, I do expect a contraction. In this scenario, our worst case would be the stock merely treading water, and the $152.57 estimate becomes a reality. The more optimistic scenario could see the stock reaching $192.92. If, however, the earnings growth accelerates and surpasses the $8 level for next year, we might witness a PE expansion, pushing the stock value beyond $215. To visualize what this means for the current options, consider the June 100 strike we previously identified at $22.92. The end-of-the-line returns could be:

In the worst case scenario we lose some of the present gains to Theta decay as the stock trades sideways, and in the better cases we could achieve further gains that would play out in the 300-400% ballpark. To me this is a hold situation. I am perfectly comfortable with risking a 25% gain (we are sitting at 153.5% gain today) to have the upside of another 150-250%. This will stay on the scoreboard!

Could Buying in Now Work?

What about buying in now? Would that work out ok? For this exercise I will give a check up on the June 2025 options since we have modeled our stock prices for that time, but I am personally more interested in having a longer runway, so I will also give some rough estimates to the December 2026 options that are now available, nearly three years from now.

June 2025 Present Option Picture:

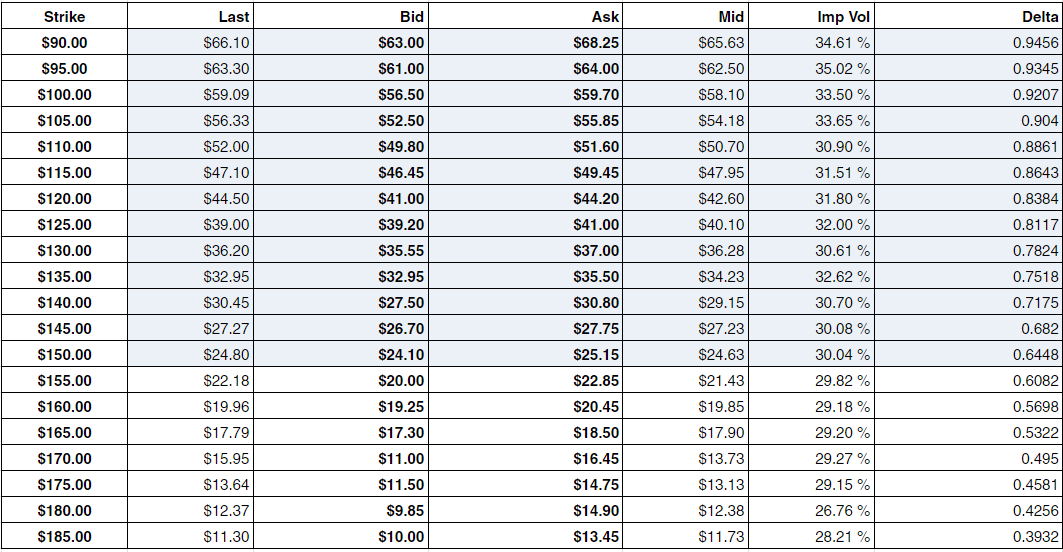

The options for June of 2025 are above, and are a bit more expensive than our last time around with an IV of 29-30%. If we used those against our modeled prices we get the monster table below:

You can see that if growth slows, buying options at the present prices will lose you a good chunk of your money. If the expectations are met then there are a few strikes for 75% returns. Should things accelerate and get better than expected we have some paths for near triples. Of these choices I would prefer the $140 strike, it is only 80% on the likely path and I normally target doubles, but this would also be in a far shorter timeline than my typical 2 year runway. One thing I don’t like however is that if things trade sideways for the next year (which could happen) 60% losses could be in store. Let’s look at the further out options that are now available and see if those are better before adding anything new to the board.

December 2026 Strikes:

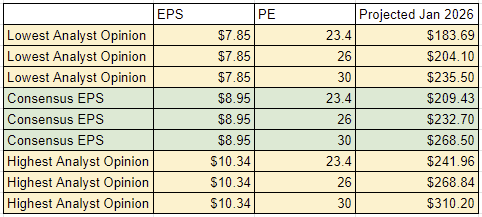

These options have a similar pricing, with an Implied Volatility (IV) of around 30%. To accurately calculate our potential returns, let's first estimate the December 2026 stock price for Google. Given its prominence, 52 analysts offer forecasts for Google’s earnings in 2025, ranging from $6.89 to $9.07, with a consensus estimate of $7.85. Factoring in an expected 19.25% growth rate for the following three quarters, the projections for December 2026 range from a low of $7.85, a consensus of $8.95, to a high of $10.34. Looking three years ahead, it’s prudent to evaluate these figures against three different Price-to-Earnings (PE) ratios: the five-year average of 23.4, the current TTM PE of 26, and, if earnings exceed $10, a potential expansion to a PE of 30, reminiscent of previous years. Taking that word soup and putting it into a chart you get:

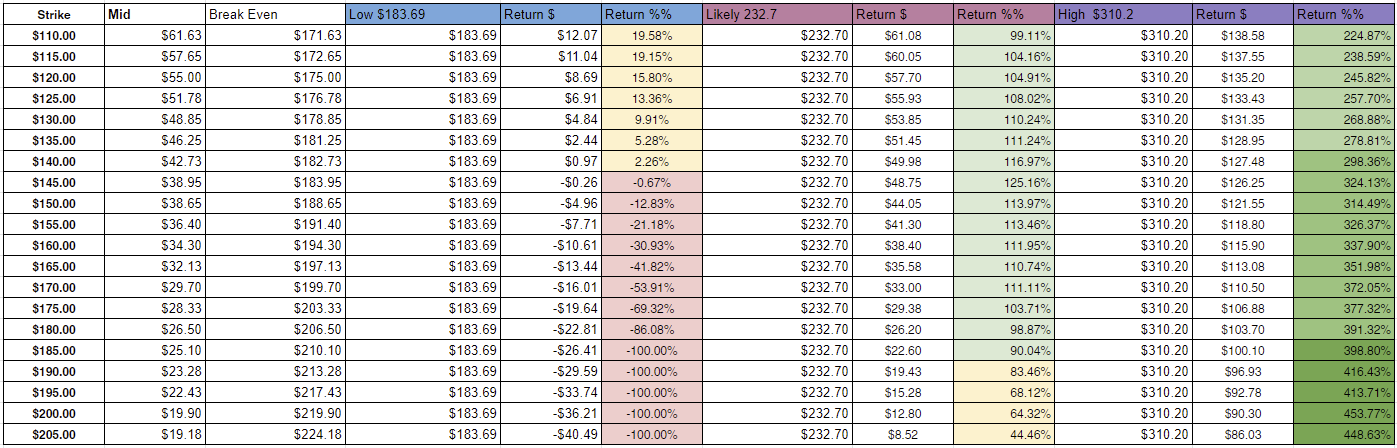

I believe that when modeling options returns for Google, it’s sensible to base our projections on a combination of PE ratios and earnings scenarios that typically occur together. Specifically, we should consider a low PE ratio alongside low earnings, as these conditions often coincide. For our consensus Earnings Per Share (EPS) estimate, we'll use a PE of 26. Additionally, should the earnings significantly exceed expectations, it's reasonable to anticipate an expansion in the PE ratio. Therefore, we'll model our returns against three scenarios: $183.69 for the low PE with low earnings, $232.70 for the consensus EPS estimate at a PE of 26, and $310.20 for scenarios where earnings significantly outperform, potentially expanding the PE. These are the benchmarks we should use to evaluate the returns for the available options:

You'll notice that in the low-end PE contraction scenario, most strikes at or near the present trading price of Google will break even. Going any more aggressive could result in significant losses. The middle path of $232 oddly winds up with most strikes having similar returns, roughly a double with a little extra jangle. In the 'Google crushes it' world of $310, there is more of a return curve, with each strike increase adding 10-20% returns. Looking at the current return/risk of the outcomes, I would consider the $145 strikes. It looks like, worst case scenario, you have a 3-year wait to break even, but it has the ability to double with what amounts to business as usual for Google. I personally think that Google is going to outpace its expectations and long-term be a winner in the AI race to come. They may not have the best chatbot, but they have the best real AI lab. This will eventually pay dividends. Should that take shape, the $140 strike gives you a quadruple. Not a bad place to be! I will add that strike to the scoreboard as another option I cover.

The last thing to consider is similar to the KMB options I wrote about a few months ago. Is a small speculation worth trying on the further out-of-the-money calls? A $200 strike option has the return profile of 50% if the stock trades at $232 in December 2026. But if things go better, it could be a 5x play. I am not sure if these are worth it the same way KMB was. Those options had really huge returns as we went down the strikes further out of the money. For Google, the closer a strike is to the current stock price, the better capital is preserved in the worst-case scenario. In the worst-case world, as we go further out of the money, each step of the way results in 10% more losses. This is offset by the best case getting 20% more as we move out. That generally doesn’t seem worth it to me, but to each their own. This is a scenario where what I view as the most likely stock price in December 2026 gives very similar returns down the strike list. So it does become up to you. Do you want more capital preserved in the worst case or more return in the best?

Other Thoughts

I really like Google. They have an AI lab that can solve real problems, and they are working on generative AI, which is so trendy. They are growing at a steady rate of 20% and are expected to continue to do so. They dominate search and are synonymous with the concept. This $1.88 trillion company has over $100 billion just sitting in cash. They have the resources, the talent, and the platform that is many people's first stop when they want to look something up. Once they fine-tune their chatbot, they will have the best position to win that portion of the AI race.

In Closing

I am adding the $145 strike for December 2026 to the scoreboard. I am not going to add any further strikes from the June 2025 list for now. They will likely yield good returns for anyone who is interested, but I prefer the plays where the worst-case scenario breaks even, and there are cases where that may not happen. I hope this gave you some ideas!

Happy Investing,

S.