Cardinal Health

I am revisiting my original Rolling Thunder positions, all of which were in Healthcare and Pharma. This predates my first newsletter by a year and a half. At that time, I identified Bristol Meyers, Merck, Cardinal Health, and AbbVie as great value speculative plays. Big tech dominated in 2021, making these giants undervalued, and the results were exceptionally positive. Subsequently, I shifted my focus to new prospects, inadvertently placing these giants on the backburner. Acknowledging that this may have taken longer than it should have, I am now reevaluating these companies. Cardinal Health is the second one I've discussed in recent weeks, and I will outline the reasons for this revisit below.

WhY?

Why consider it? In all seriousness, it's because it's a remarkable company that has consistently shown robust growth, and this trend is expected to persist. Revenues have experienced a year-over-year growth of 8%, reaching 12% this past year, accompanied by a corresponding increase in earnings. While it averaged around 4% over the past few years, recent figures show a notable acceleration to 11%, with projections indicating an impressive 17% growth over the next 3-5 years, as per insights from 16 analysts.

Just yesterday, the company released guidance forecasting year-end earnings between $6.75 and $7.00 per share, reflecting a remarkable 20% year-over-year growth. Despite this positive news, the market exhibited a lukewarm response, leading to a dip in the stock. Perhaps some of the skepticism is rooted in the company's stated goal of achieving 12-14% growth in the upcoming years, slightly below the optimistic 17% predicted by analysts.

Closing the day at around $103 per share, the company is currently trading at 14.71 to 15.26 earnings. This presents a compelling bargain for a company exhibiting such robust growth.

Recent Performance

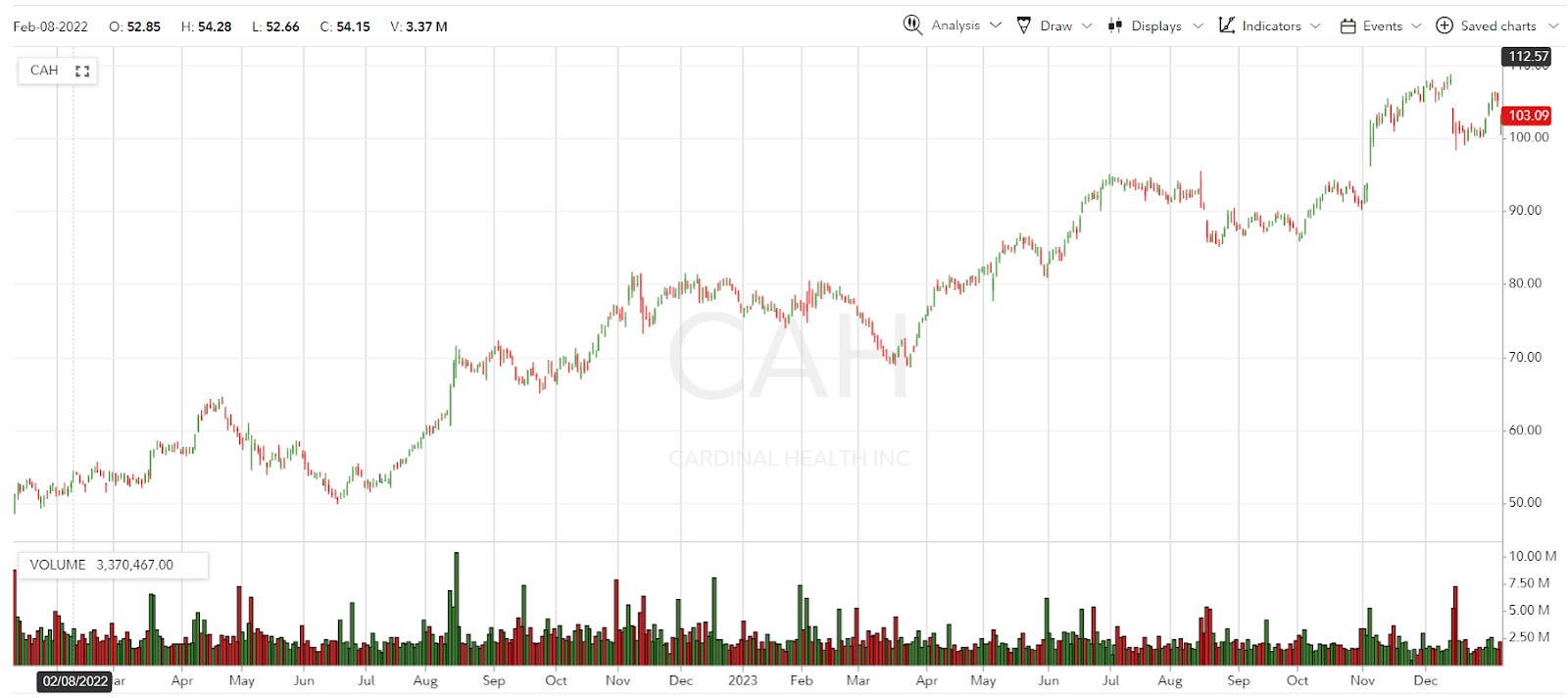

It has been a fantastic 5 years for Cardinal Health, soaring from just under $50 a share to yesterday's closing at ~$103. Doubling in value over 5 years equates to an impressive ~14% annual return rate. That is quite substantial. If the company manages to achieve the projected growth of 14% per year, it should also translate into a minimum of 14% annual stock price appreciation, contingent on the valuation.

Valuation

How should we assess the value of CAH? It carries a substantial amount of debt, which is consistent with its industry peers. The company is experiencing robust growth. However, due to one-off expenses and the uncertainties surrounding the COVID market, determining a normal PE ratio becomes challenging. In the period post-financial crisis and pre-COVID, the stock typically traded within the range of 14 to 19, which seems reasonable, albeit with occasional deviations.

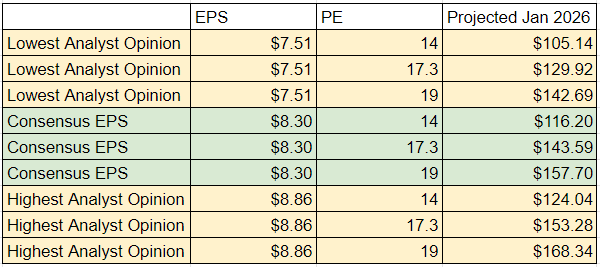

Drawing inspiration from Peter Lynch's approach outlined in "One Up on Wall Street," where he often suggested the fair PE ratio to be the company's growth rate, we arrive at a figure of 17.3 if the company continues its projected growth. To model LEAPs effectively, we should look ahead to 2026 and evaluate the company using three distinct PE ratios: 14, 17.3, and 19.

Projections

According to 16 analysts, CAH is projected to generate $7.69 (with a low estimate of $6.96 and a high of $8.20) for the fiscal year ending in June 2025. This provides them with a couple more quarters of potential growth before the LEAPs expire. If we extrapolate the expected growth rate of 14-17% for the next two quarters, we could anticipate trailing twelve-month (TTM) earnings ranging from $8.15 to $8.30 (with a low estimate of $7.51 and a high of $8.86) by the year's end. Considering the company's stated guidance, the higher end of this range may seem less likely, while the lower end becomes more plausible if things don't progress optimally. Utilizing the PE ratios discussed earlier and these EPS estimates, we can project the potential stock value in 2 years:

If the company continues its growth towards that $8.30 ballpark, I doubt the PE will remain at 14. However, it could happen if the future appears less than bright at that time.

The Options

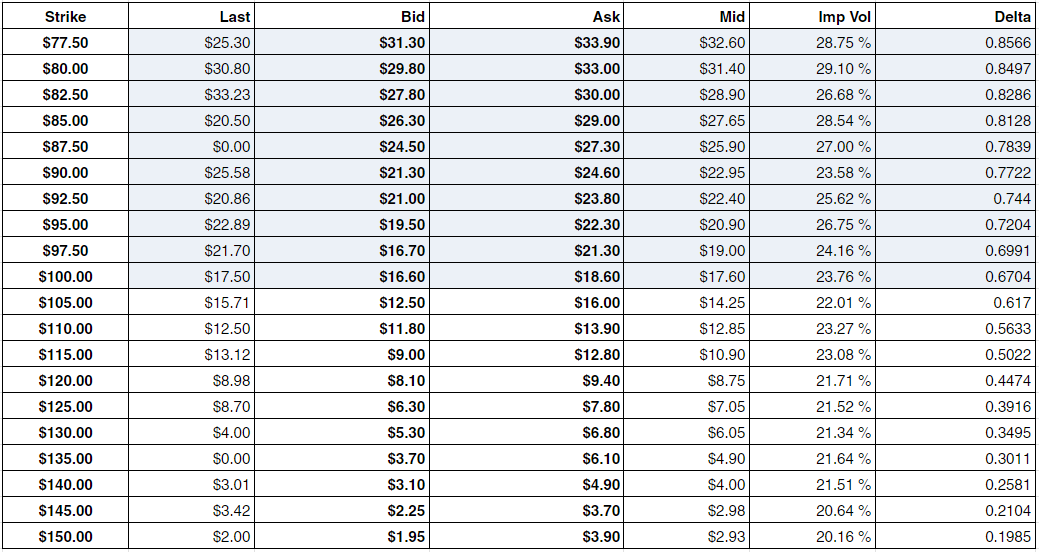

Close of market yesterday brought us options priced like this:

Great. Low IV is good. A few out of the money strikes have a Delta above 0.5, that is good. Against our price predictions what do we see for returns? *Big chart siren blares*

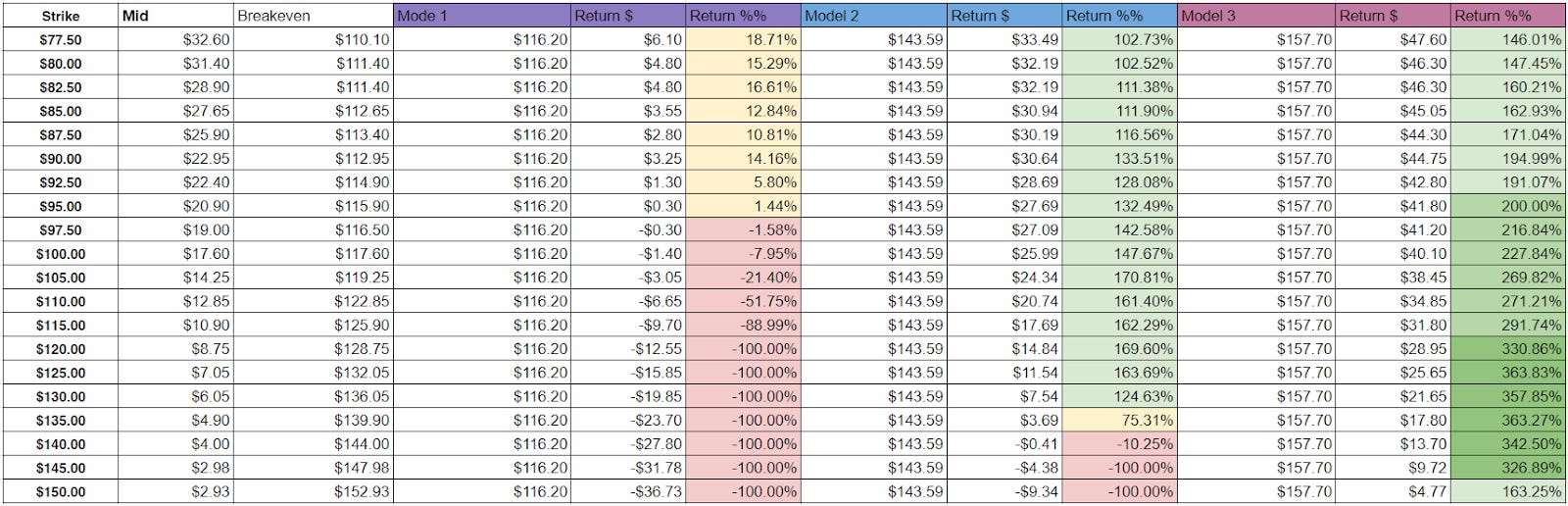

In a scenario where growth is sluggish, and the PE contracts to 14 with earnings reaching $8.30, we observe that the in-the-money strikes yield low returns, essentially providing a return of your initial investment. At this point, it becomes more advantageous to simply purchase the underlying stock. The situation improves significantly if the PE expands in tandem with sustained growth. In a world where the stock is trading in the $140-160 range, more outcomes offer substantial returns.

I would feel comfortable considering anything up to the $125 strike. Beyond this point, in the realm of a $143 CAH, returns start to diminish, even though the higher valuation world might offer more upside. The $105 strike is where returns climb to approximately 170%. For our scoreboard, let's use the $105 strike as it encapsulates most of the significant return potential found in higher-strike options, with a comparatively minimal loss (21%) in case things take a downturn. Choose the option that aligns best with your preferences!

Happy investing,

S.